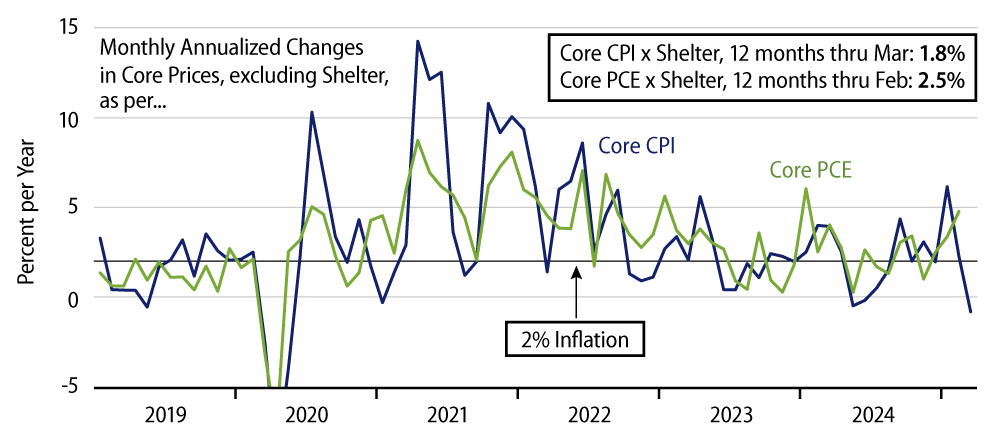

The headline Consumer Price Index (CPI) declined -0.1% in March, or at an annualized monthly rate of -0.6%. Upon excluding food and energy, the core CPI rose 0.1%, or at an annualized monthly rate of 0.7%. Due to vagaries in the Labor Department’s reporting of shelter costs, we have been tracking a core CPI measure that excludes shelter costs. That measure declined -0.1% in March, or at an annualized rate of -0.9%.

Needless to say, the March consumer price news offered welcome relief following above-trend inflation prints in January and February. Maybe pricing conditions changed abruptly in March. Maybe we were right that the January/February prints reflected prices adjustments following the Fall hurricanes. Maybe this is all random fluctuation. Whatever the explanation, the fact remains that for the last 12 months as whole, core CPI inflation excluding shelter is now only 1.8%, just below the Fed’s 2.0% target.

Yes, the Fed’s target actually pertains to the core Personal Consumption Expenditures (PCE) price index, and March data for that measure is not yet available, but as we’ll detail in the following, the expectation is that core PCE will be similarly restrained in March. And, yes, shelter costs are still elevated, so that the core CPI including shelter rose at a 2.8% rate over the last 12 months.

However, as we have detailed before, shelter costs have been much better behaved in recent months than they were prior to August 2024. In other words, the 12-month inflation rate for shelter is still held up by its high monthly prints in early 2024, and as we move ahead, that 12-month shelter inflation rate can be expected to roll down considerably, working to pull the overall core CPI down with it.

With respect to the core PCE index, many of its components mirror the changes in CPI components, but with different weights. Thus, the weight for shelter costs in the core PCE is only 18%, compared to a 42% weight in the core CPI. Given that shelter accounted for more than all of the increase in the core CPI in March, just the lower weight for shelter in the core PCE will work to pull down that aggregate, and we believe that other components will work similarly.

Of course, while today’s news essentially negates the inflation news of the prior two months, the markets’ fixation is on tariffs. There is no way we could or would want to construe tariffs as good news for inflation. However, a monetary approach would dictate that tariffs would be more of a negative for the economy than for inflation. Similarly, service prices will be affected by tariffs only to the extent that service providers use newly purchased goods to produce their services. There should be even less effect on shelter costs.

This perspective is unlikely to sway market sentiment in the short term, but it would be relevant when and if that perspective takes hold in actual market prices. Meanwhile, we can hope that trade deals are reached that do serve to alleviate the financial markets’ fears. In the meantime, we’ll find what consolation we can in the fact that actual price conditions look much better today than was the case a month ago.