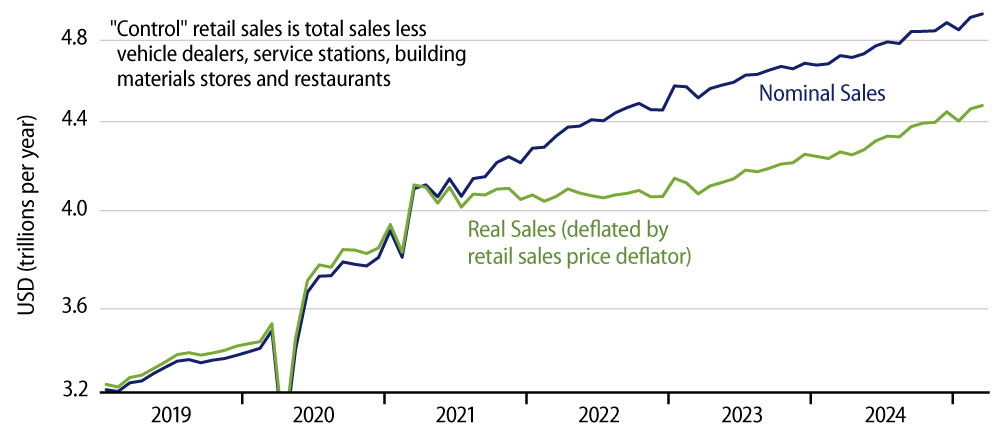

Headline retail sales rose 1.4% in March, with the February sales estimate revised upward by 0.3%. The more closely watched ''control'' sales estimate rose 0.4%, with a large +0.5% revision to the February sales estimate. (Control sales abstract from sales at car dealers, service stations, building material stores and restaurants, so as to focus on store types that are more frequented by consumers rather than businesses.)

These March sales gains, along with similar gains in February, contradict the claims of consumer weakening that surrounded the January sales data two months ago. Even at that time, our take was that the declines in sales announced for January likely reflected “seasonal noise” coming off the 2024 Christmas holiday season. The last two sales reports have fully confirmed that take. As Exhibit 1 makes clear, the January sales declines were not that large to begin with, and the February/March gains fully restore the growth trend that was in place over 2023-2024.

This is important because the recession talk that has been helping roil financial markets recently got its start in the January retail sales report. Granted, the trade wars have fanned that fury, but even Chicken Little needed an actual acorn hit to start his fears. Consumer weakness was the acorn for the recession crowd, but it has now essentially vanished from the data. Recession fears may not vanish as well, but they are now fully based on prospective events, not on anything in the data at hand.

The sales rebound of the last two months was focused in retailers of nondurables, such as online vendors, department stores and grocers. Sales at durable goods retailers continue to be generally sluggish, as has been the case for the last two years, although there has been a mild bounce at car dealerships recently.

So, no, consumer spending is not booming, and there are continued strains for brick-and-mortar retailers, as online sales continue to gain market share. However, again, these ''downsides'' have been in place for quite some time. Meanwhile, there is no recent net slowdown in any major retail sector, contrary to what some pundits were claiming two months ago.