Macros, Markets and Munis

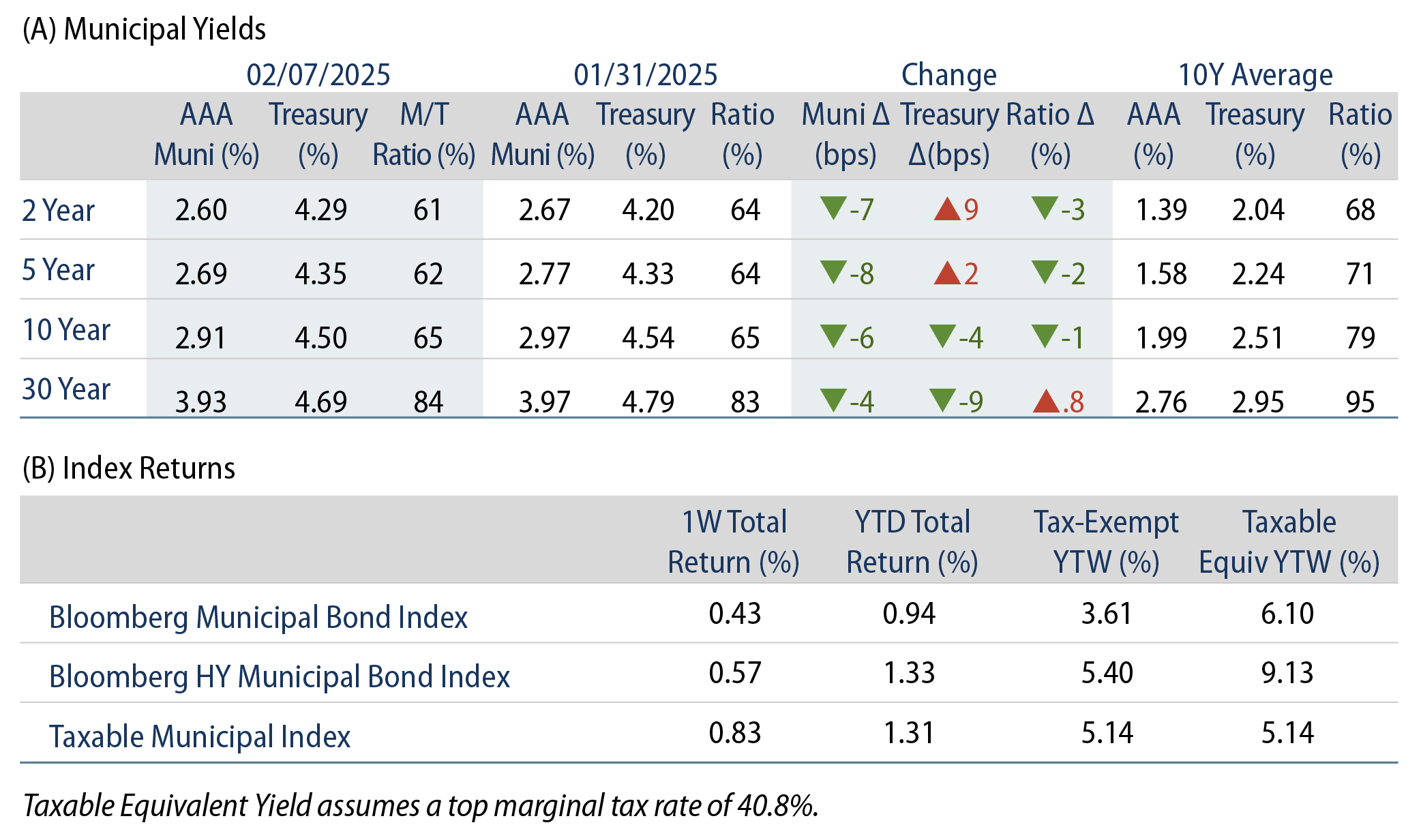

Munis posted positive returns last week as fund flows remained positive amid elevated supply conditions. The Treasury curve flattened amid generally weaker economic data. December job openings declined and came in lower than expected earlier in the week, followed by weaker durable goods orders and University of Michigan sentiment data. January nonfarm payrolls data also declined and was below expectations, but this weakness was offset by upward revisions to the prior month that painted a more favorable picture for labor markets. Muni yields moved lower across the curve, outperforming the flattening trend observed in Treasury markets. The Bloomberg Municipal Index returned 0.43% during the week, the High Yield Municipal Index returned 0.57% and the Taxable Municipal Index returned 0.83%.

Technicals Remained Characterized by Elevated Supply and Demand

Fund Flows (up $1.1 billion): During the week ending February 5, weekly reporting municipal mutual funds recorded $1.1 billion of net inflows according to Lipper. Long-term funds recorded $534 million in inflows, intermediate funds recorded $228 million of inflows, and high-yield funds recorded $330 million of inflows. Last week’s inflows led year-to-date (YTD) inflows higher to $5 billion.

Supply (YTD supply of $46 billion, up 11% YoY): The muni market recorded $12 billion of new-issue supply last week, up 39% from the prior week. The market has also recorded $46 billion of new issuance YTD, up 11% year-over-year (YoY). This week’s calendar issuance is expected to decline to $8 billion. The largest deals include $1.3 billion New York City Transitional Finance Authority and $650 million Salt River Project Agricultural Improvement and Power District transactions.

This Week in Munis: Supply Starts Strong

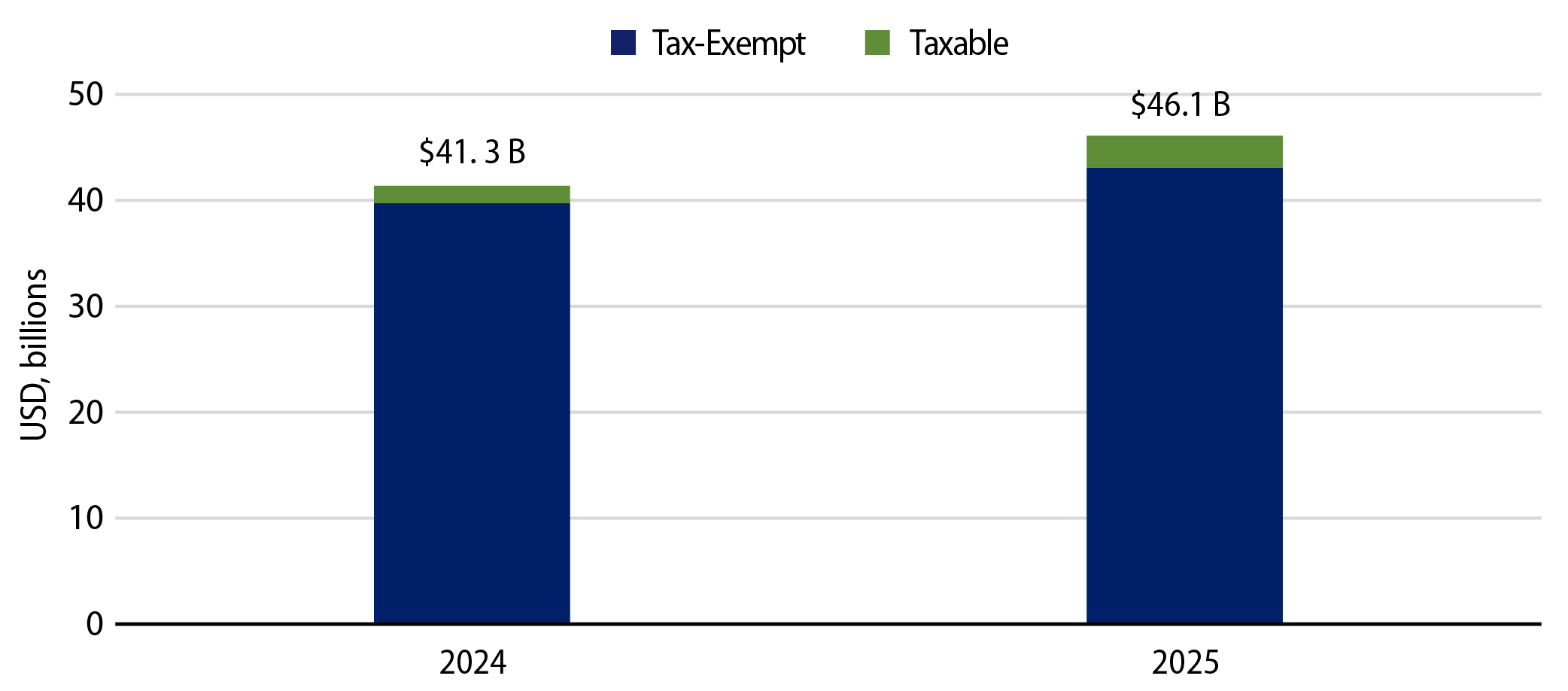

Entering 2025, market participants questioned whether municipal supply could keep up the record pace observed in 2024, particularly amid potential policy uncertainty associated with the new administration. New issuance trends observed so far this year have exceeded the record pace observed in 2024. According to Bloomberg, YTD supply through February 7 reached $46 billion, up 11% YoY. Tax-exempt issuance is 8% higher at $44 billion YTD, while taxable issuance (including corporate CUSIP) has nearly doubled YoY to $3.0 billion.

Taxable and Tax-Exempt Issuance

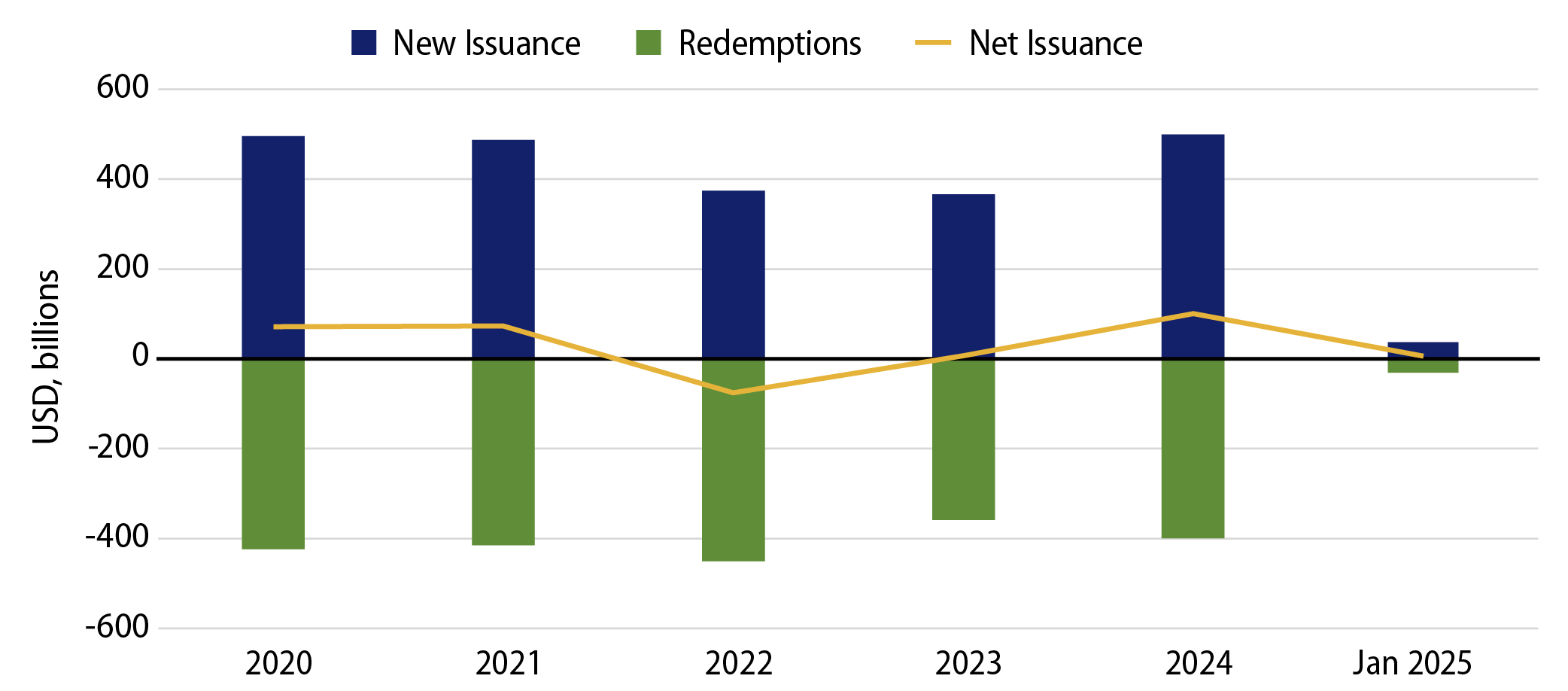

A potential distinction of 2025 supply versus the prior record year could be the breakdown of new money versus refunding issuance. A key driver of the record 2024 issuance was elevated refunding activity, partially driven by issuers redeeming legacy taxable debt for more favorable financing rates in the tax-exempt market. Bond Buyer data indicates that refunding volume increased 76% in 2024 to $152 billion, or 30% of total issuance. In January, only 17% of issuance was dedicated to refunding activity, with 83% of issuance characterized as new money financing.

The current pace of supply outpacing the prior year bodes well for investors seeking to capitalize on the relatively higher tax-exempt income opportunities offered in the market, particularly if demand remains positive or accelerates as the curve normalizes. The fact that more issuance is coming to market to fund new projects versus refunding volume (which has less of an impact on the stock of outstanding muni supply) bodes well for more positive net supply trends and overall municipal market opportunities.

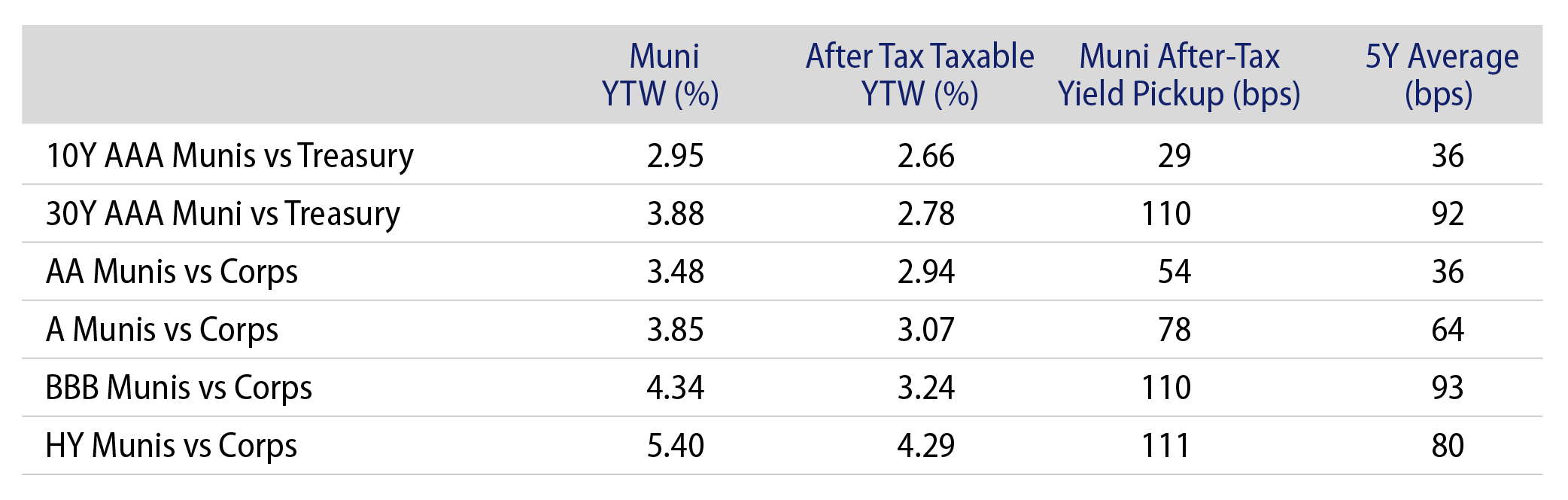

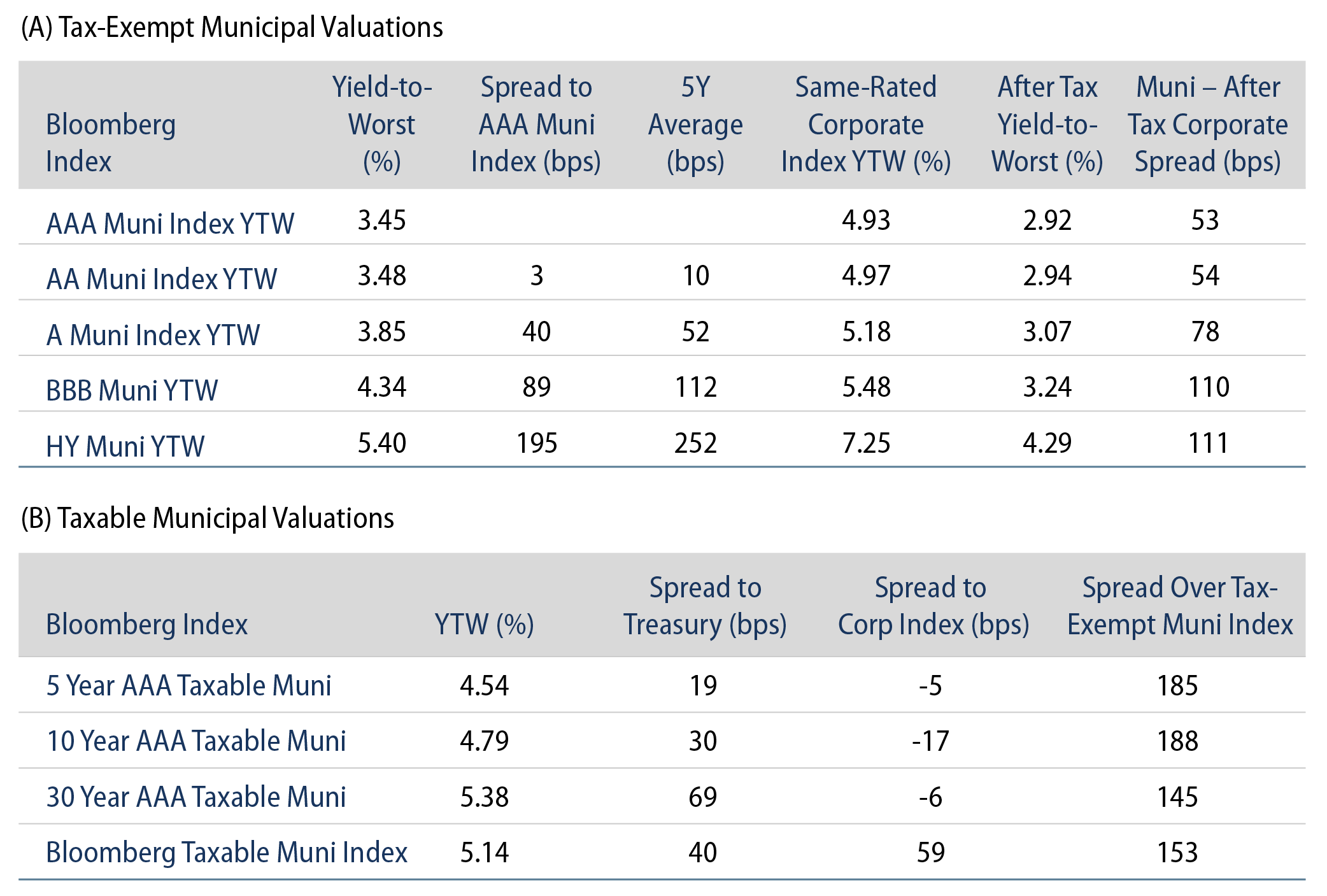

Municipal Credit Curves and Relative Value

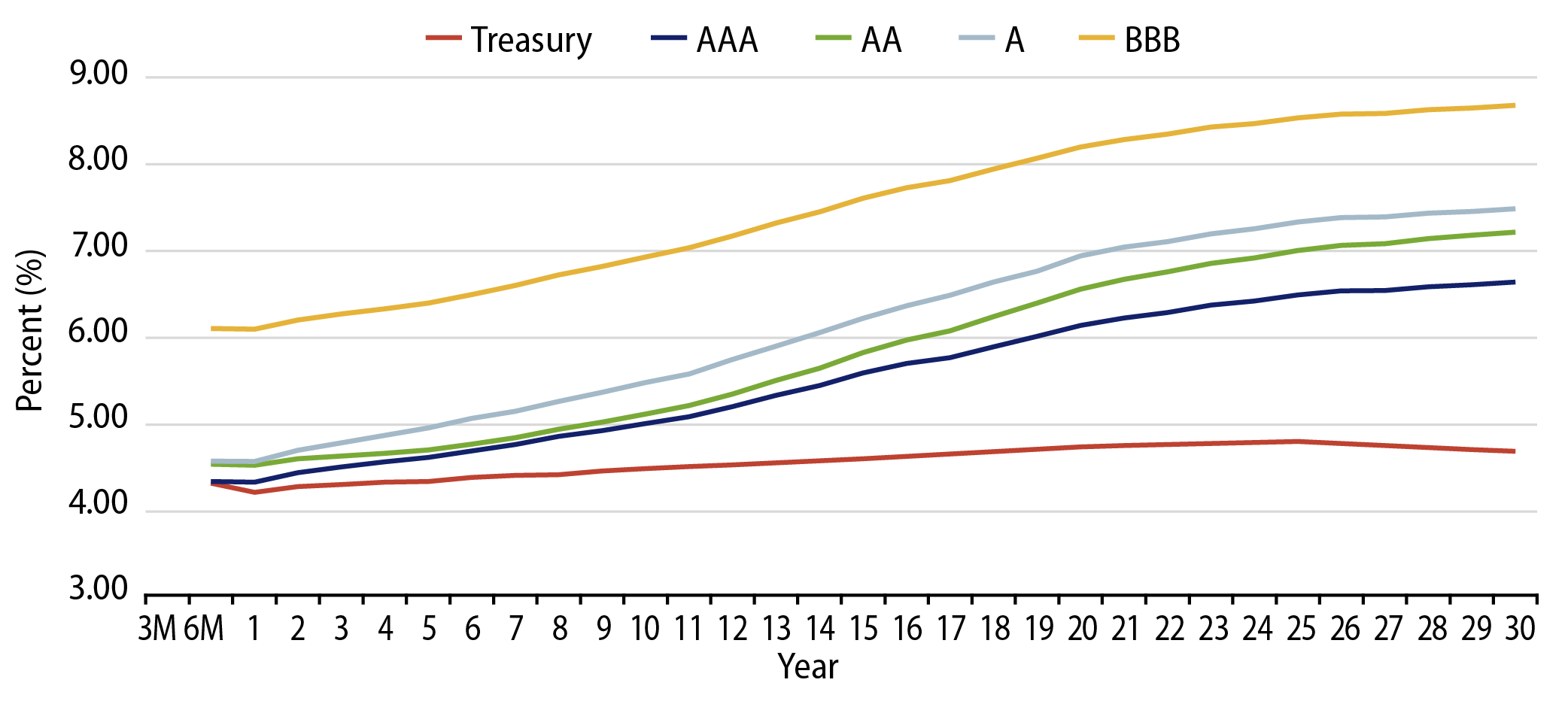

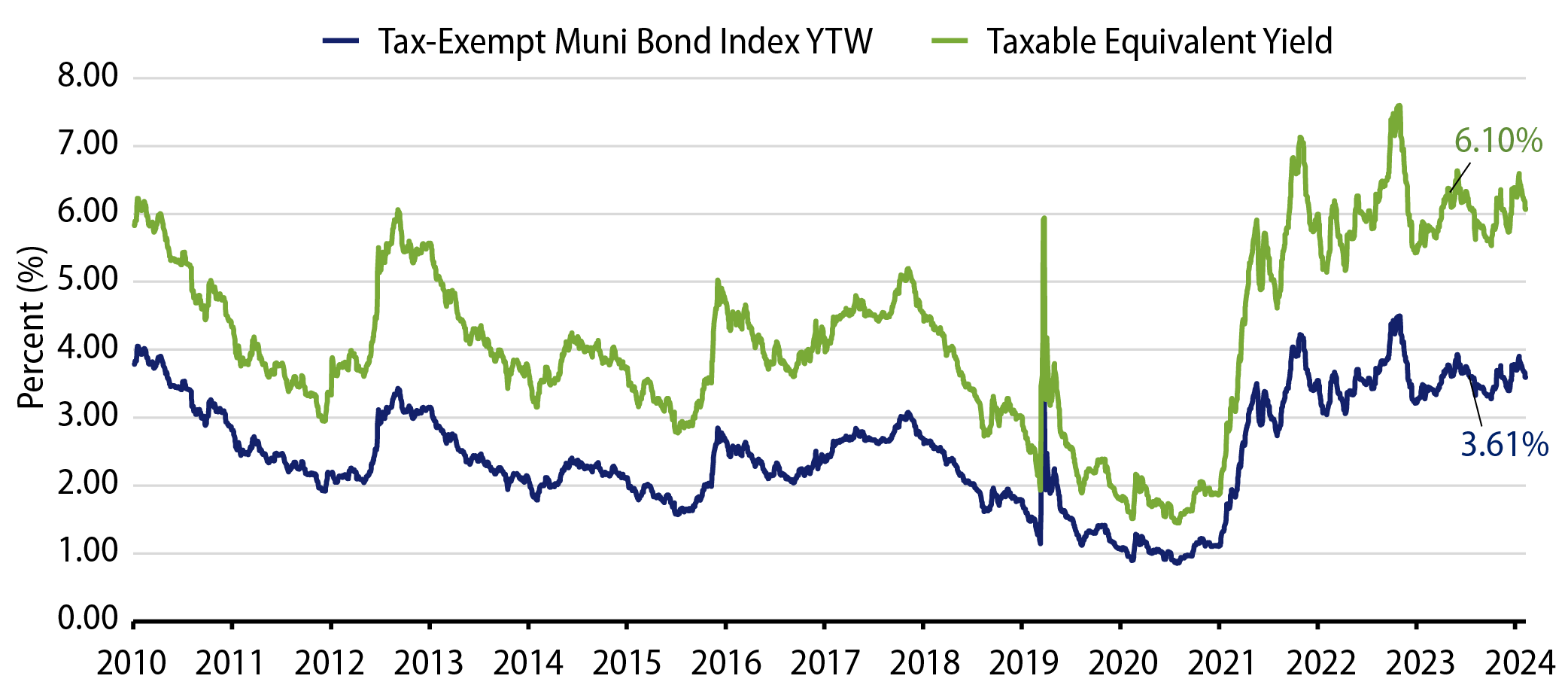

Theme #1: Municipal taxable-equivalent yields and income opportunities remain above decade averages.

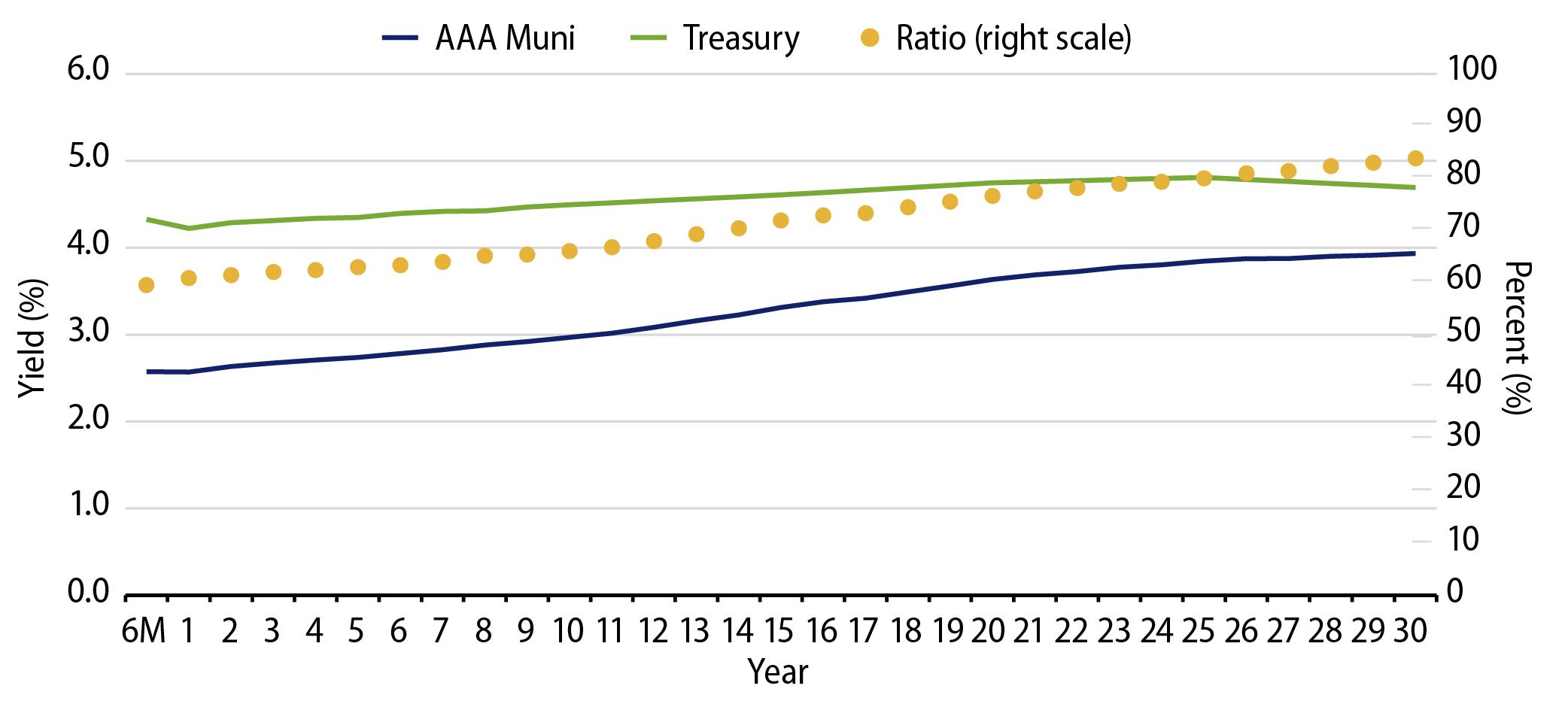

Theme #2: The muni curve has steepened, offering better value in longer maturities.

Theme #3: Munis offer attractive after-tax yield pickup versus longer-dated Treasuries and investment-grade corporate credit.