Macros, Markets and Munis

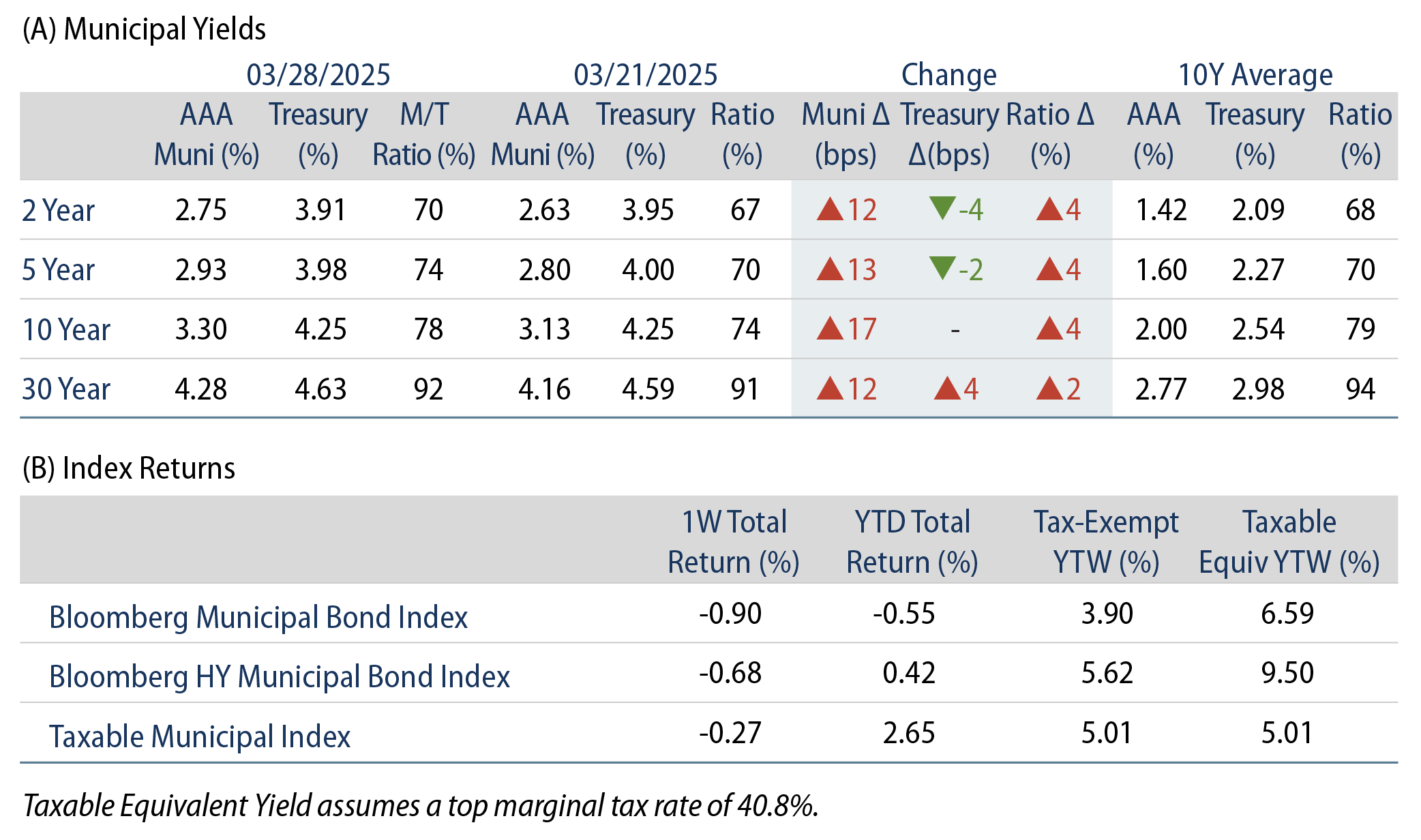

Munis posted negative returns last week as the Treasury curve steepened, moving 2-4 basis points (bps) higher in shorter maturities and 4 bps higher in longer maturities. Financial markets were on edge throughout the week ahead of the Trump administration’s expected April 2 tariff deadline. Economic data came in weaker than expected as employment remained unchanged, but consumer confidence and sentiment indicators were reported below expectations. Core Personal Consumption Expenditures (PCE), the Federal Reserve’s (Fed) preferred inflation gauge, also moved higher to 2.8%. Meanwhile, municipals sold off across the yield curve and underperformed amid weaker technical conditions as mutual funds posted outflows for a third straight week. This week we highlight the shifts in municipal demand observed in 2024.

Elevated Supply and Fund Outflows Challenged Technicals

Fund Flows (down $573 million): During the week ending March 26, weekly reporting municipal mutual funds recorded $573 million of net outflows, according to Lipper. Long-term funds recorded $383 million of outflows, intermediate funds recorded $34 million of outflows and high-yield funds recorded $148 million of inflows. Last week’s outflows marked a third consecutive week of net outflows amid the seasonal tax-season weakness and led year-to-date (YTD) inflows lower to $10 billion.

Supply (YTD supply of $122 billion; up 36% YoY): The muni market recorded $9 billion of new-issue supply last week, down 17% from the prior week. YTD, the muni market has recorded $122 billion of new issuance, up 34% year-over-year (YoY). Tax-exempt and taxable issuance are up 36% and 44%, respectively, though tax-exempt issuance has comprised the vast majority (94%) of YTD supply. This week’s calendar is expected to increase to $12 billion. The largest deals include $1.3 billion state of California general obligation and $600 million University of Southern California transactions.

This Week in Munis: Shift in Muni Debt Holders

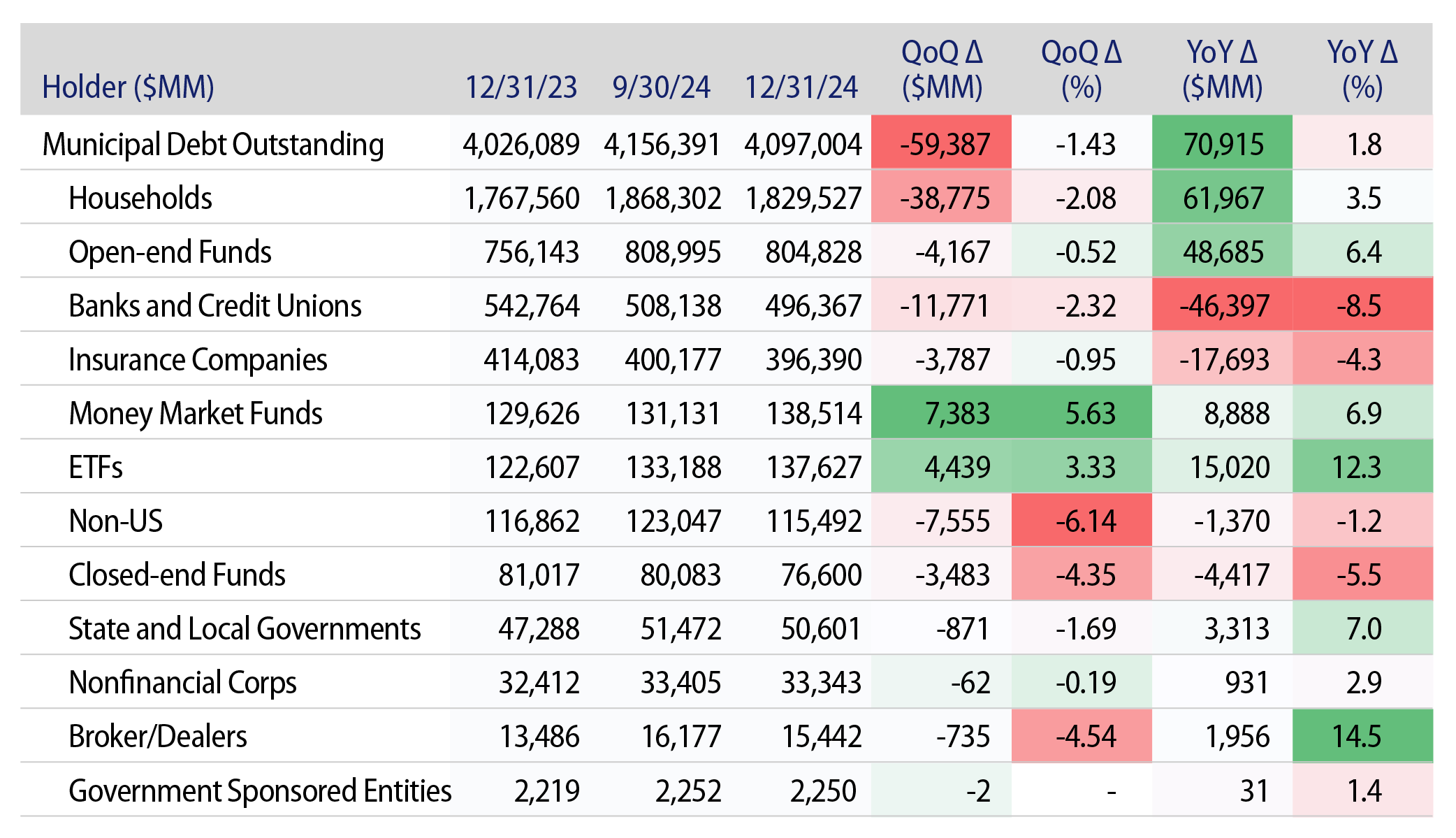

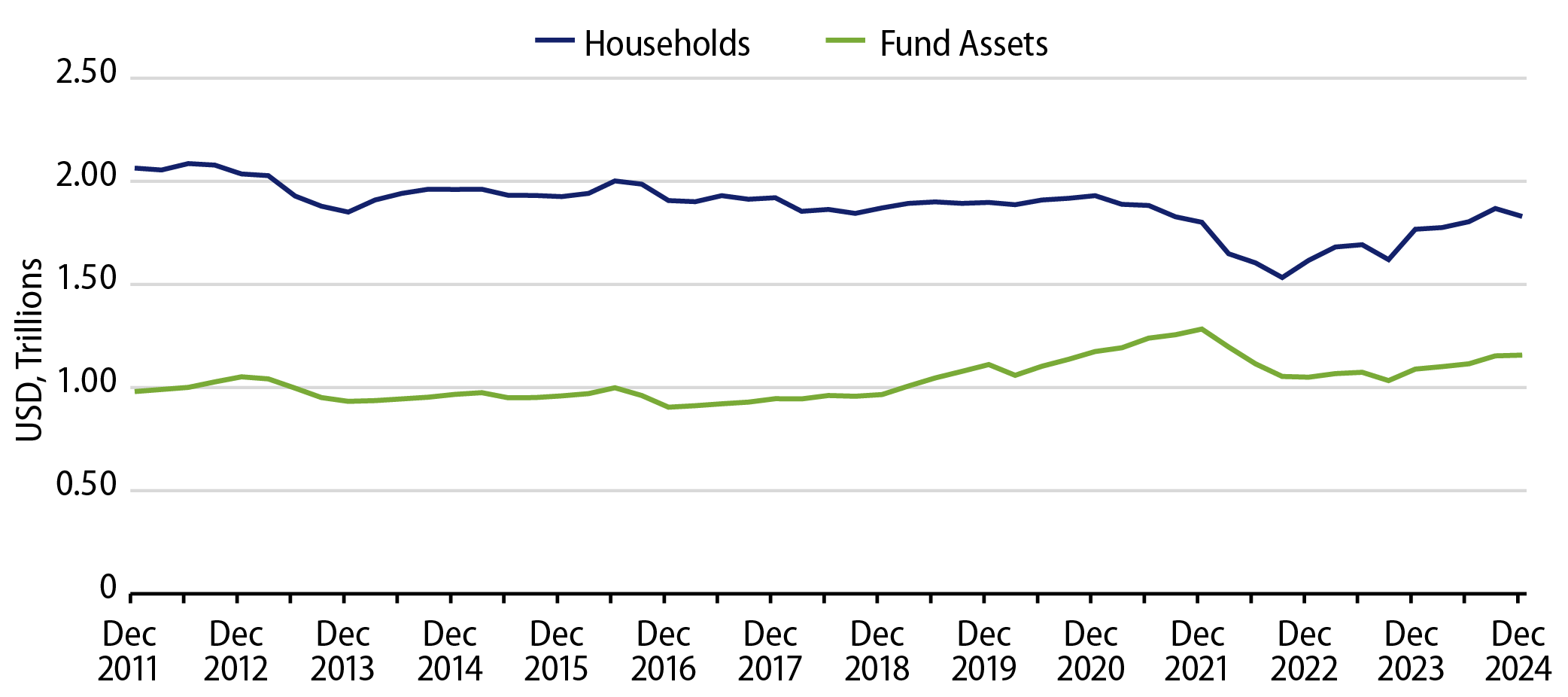

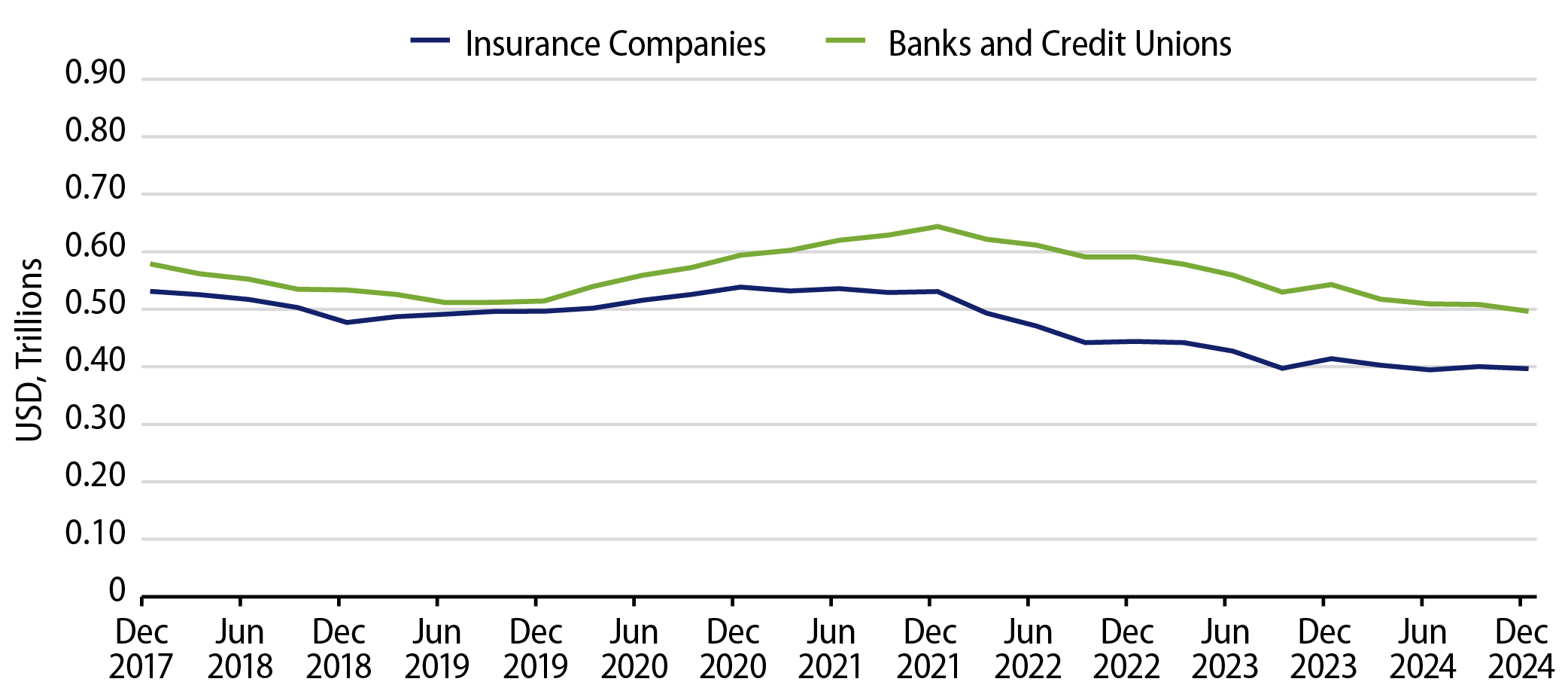

Earlier this month, the Fed released its updated Flow of Funds data, highlighting the primary holders of municipal debt through the end of 2024. According to the data, throughout the year municipal holdings continued to grow among retail individual holders, while holdings among major institutional holders (banks and insurance companies) declined.

The municipal holdings data indicated $131 billion (+4.6%) growth across fund and separately managed account (SMA) vehicles in 2024. Total household holdings, a proxy for SMA demand, increased by $62 billion (+3.5%) during the year as the SMA vehicle remained an attractive solution for investors seeking customized objectives within a muni allocation. Municipal fund assets increased $68 billion (+6.3%) during the year. Open-end funds, ETFs and money market funds increased $49 billion (6.4%), $15 billion (12.3%) and $9 billion (6.9%) during the year, respectively.

Institutional holdings of municipal debt declined $64 billion (-6.7%) during the year, attributable to lower corporate tax rates, increased tender/call activity of taxable municipal debt and bank balance sheet de-risking of longer-duration municipal assets. Insurance company holdings of municipals declined by $17 billion (-9%) in 2024. Bank municipal holdings decreased by $46 billion (-9%) during the year. Non-US demand for taxable municipals also declined 1% in 2024.

The Fed data underscored the growth of the overall municipal asset class last year, as well as the increasing demand from individual investors subject to higher tax rates. However, institutions stepped away as marginal buyers of traditional tax-exempt municipals, leading to a higher concentration of traditional retail individual investors within the market. Western Asset believes that the less diversified demand base of the muni market could contribute to volatility but also create opportunities for an active manager in these uncertain market conditions.

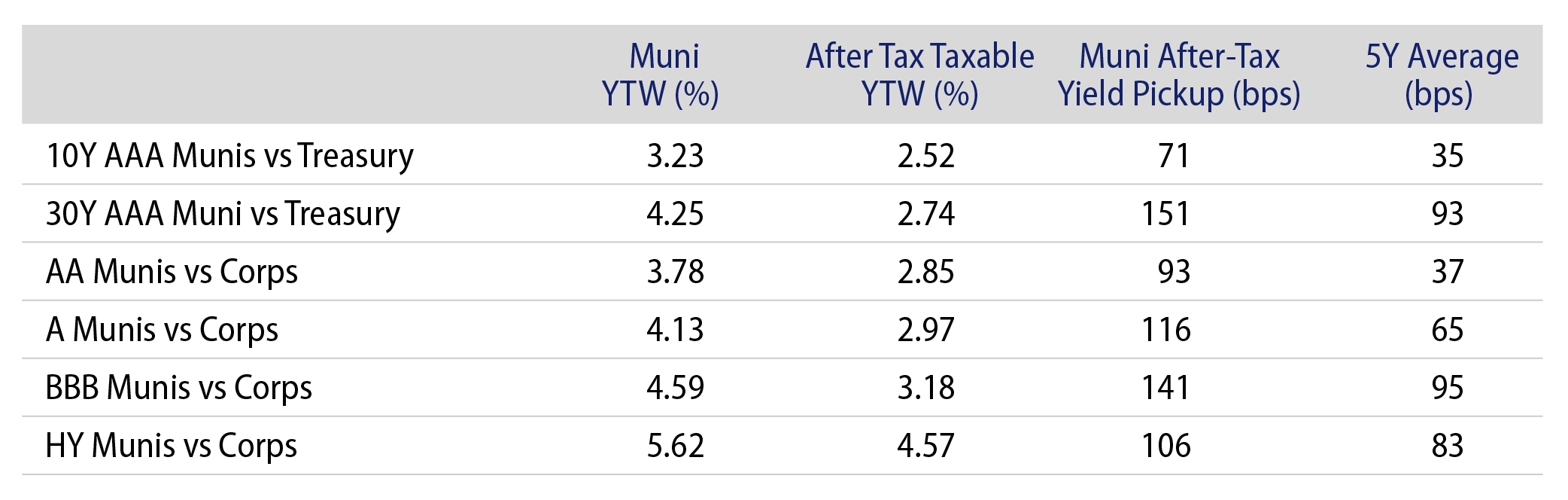

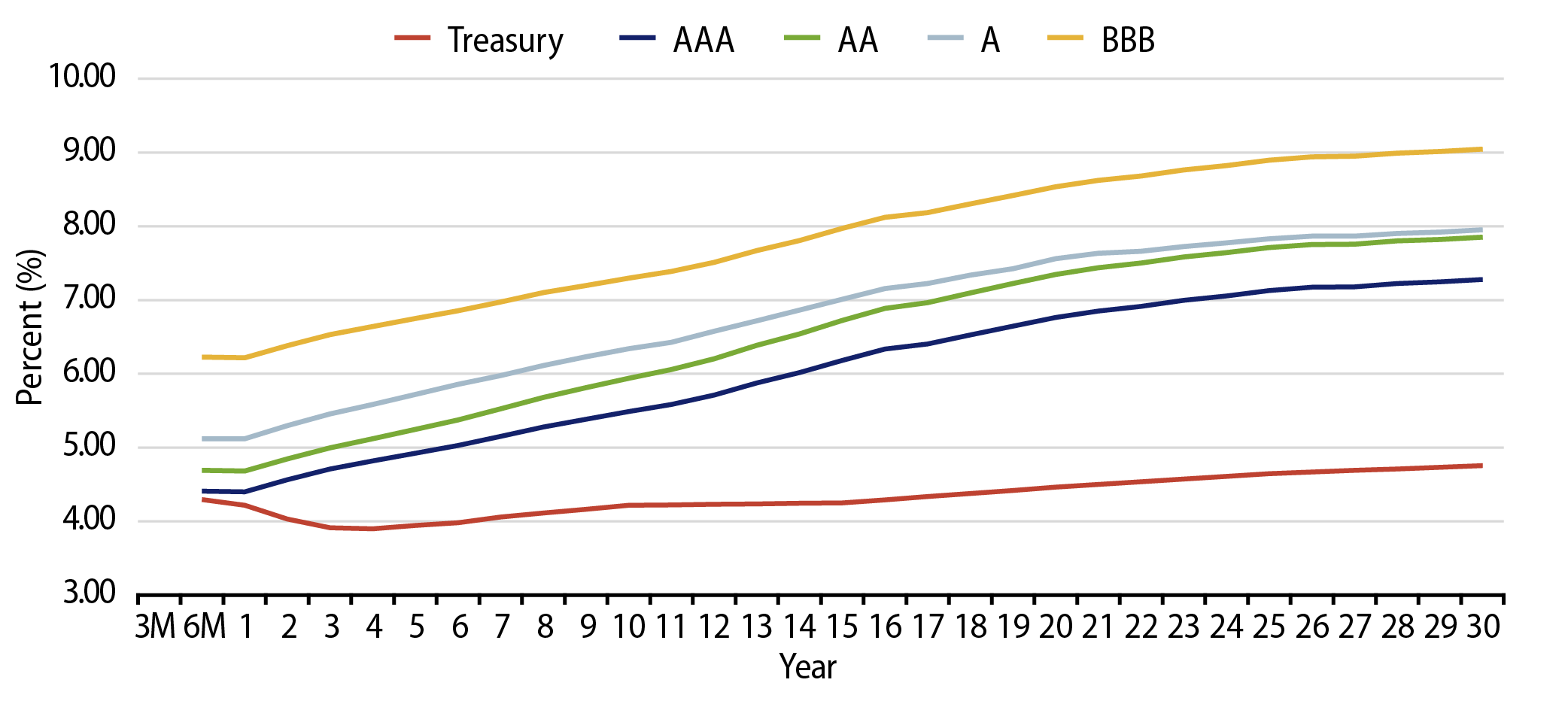

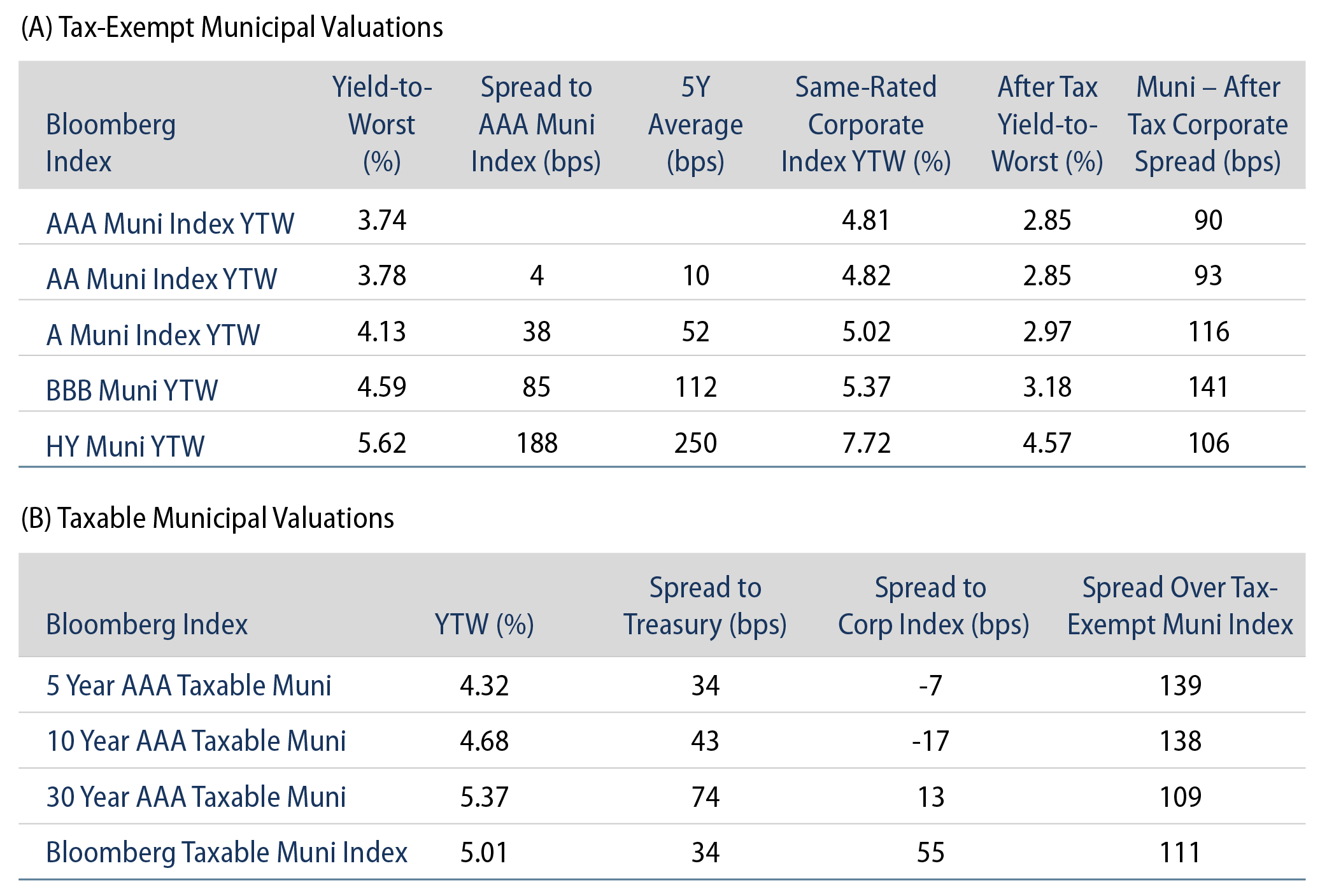

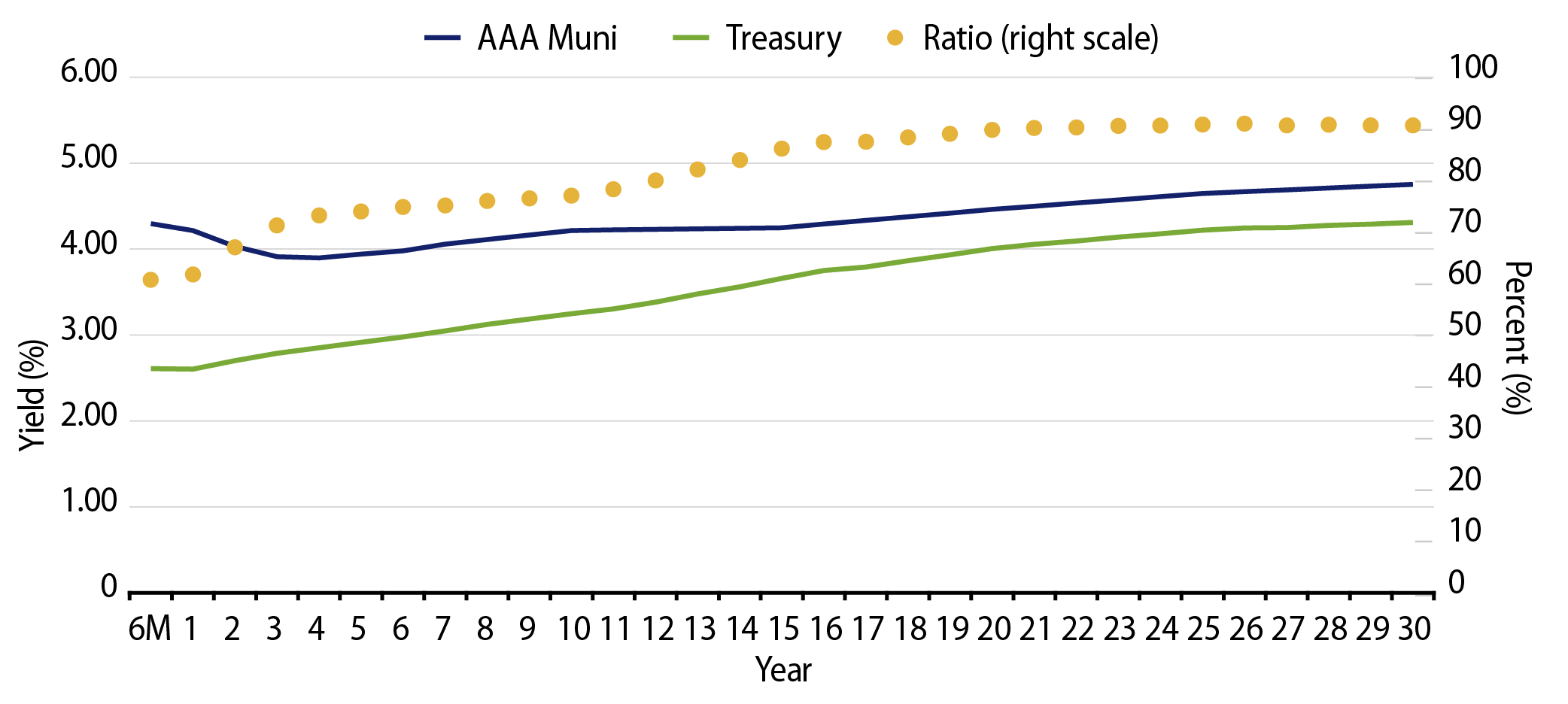

Municipal Credit Curves and Relative Value

Theme #1: Municipal taxable-equivalent yields and income opportunities remain above decade averages.

Theme #2: The muni curve has steepened, offering better value in intermediate and longer maturities.

Theme #3: Munis offer attractive after-tax yield pickup versus longer-dated Treasuries and investment-grade corporate credit.