Private-sector payrolls rose by 209,000 jobs in March, with that decent gain offset only slightly by a -26,000 revision to the February jobs estimate. Meanwhile, average workweeks were unchanged, while average hourly earnings rose a scant 0.25%, or at an annualized rate of 3.1%. (The Federal Reserve (Fed) has judged 3.5% average wage growth as being consistent with its 2% inflation target.)

The payroll data were favorable by any perspective we can conceive of. The trend of slowing job growth evident in 2022 and 2023 has been fully stemmed—at least, for now, and some sectors of the economy are actually showing better job growth in recent months than they were in 2024. Declines in the workweek in December and January that held down gains in total hours worked were reversed in February and March. Finally, wage growth has been consistent with Fed inflation targets for four months now. As we have heard from others this morning, this is about as close to a Goldilocks release as one could hope for.

We emphasize this because so many analysts have been touting/seeing weakness developing in the economy in recent months, even ahead of any putative negative effects of the trade wars. At this point, the touted weakness is contained solely in the January/February consumer spending data, and as we have detailed in past posts, even that data shows only a mild slowing in growth, rather than worrisome declines. Furthermore, as we have also stated before, the softer consumer spending prints may be partly due to seasonal effects coming off strong holiday spending in late 2024.

Elsewhere, the economy actually held up much better than we were expecting, and today’s payroll report is right in line with those trends. Of course, this is history, and the financial markets are roiling due to fears about how the future economy might react to tariffs foreign and domestic. Still, past is prologue, as the saying goes, and while we fret about how things may develop, it is worth keeping in mind that at least given the data in hand, weakness or weakening has been scarce.

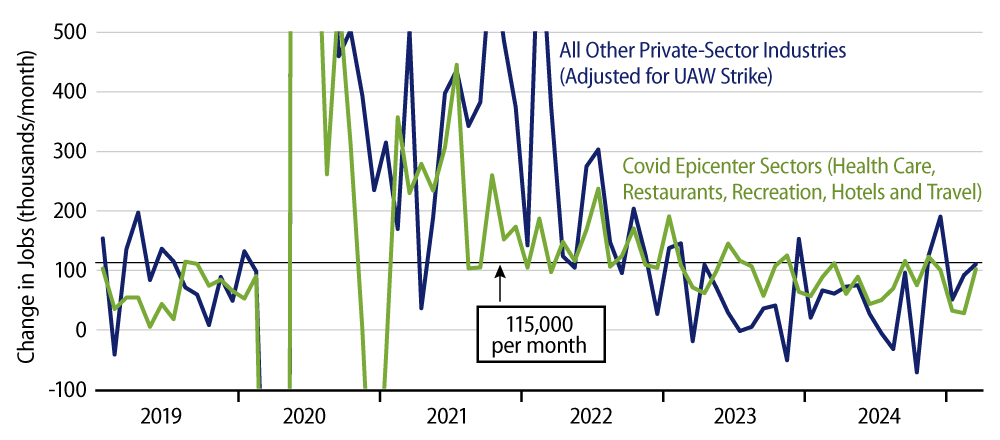

Exhibit 1 provides a pithy depiction of payroll job trends. Sectors especially hard hit by the Covid shutdown five years ago had seen some slowing in job growth in January and February. However, these sectors rebounded nicely in March. Meanwhile, the rest of the economy had actually seen better job growth since November, and this continued to be the case in March. Combine continued better job growth in most sectors with a March rebound in Covid-affected sectors, and you get the improvement in growth registered by total private-sector payroll jobs in March.