Private-sector payroll jobs rose by 140,000 in February, offset slightly by a -16,000 revision to the January print, according to data released today by the Labor Department. In other facets of the report, workweeks were shorter over the last three months, so that total hours worked were down over that span. Average hourly wages rose a modest 0.28% in February, and growth there has been consistent with the Federal Reserve’s (Fed) inflation targets for a few months now. The unemployment rate ticked up very slightly to 4.1% from 4.0% in January.

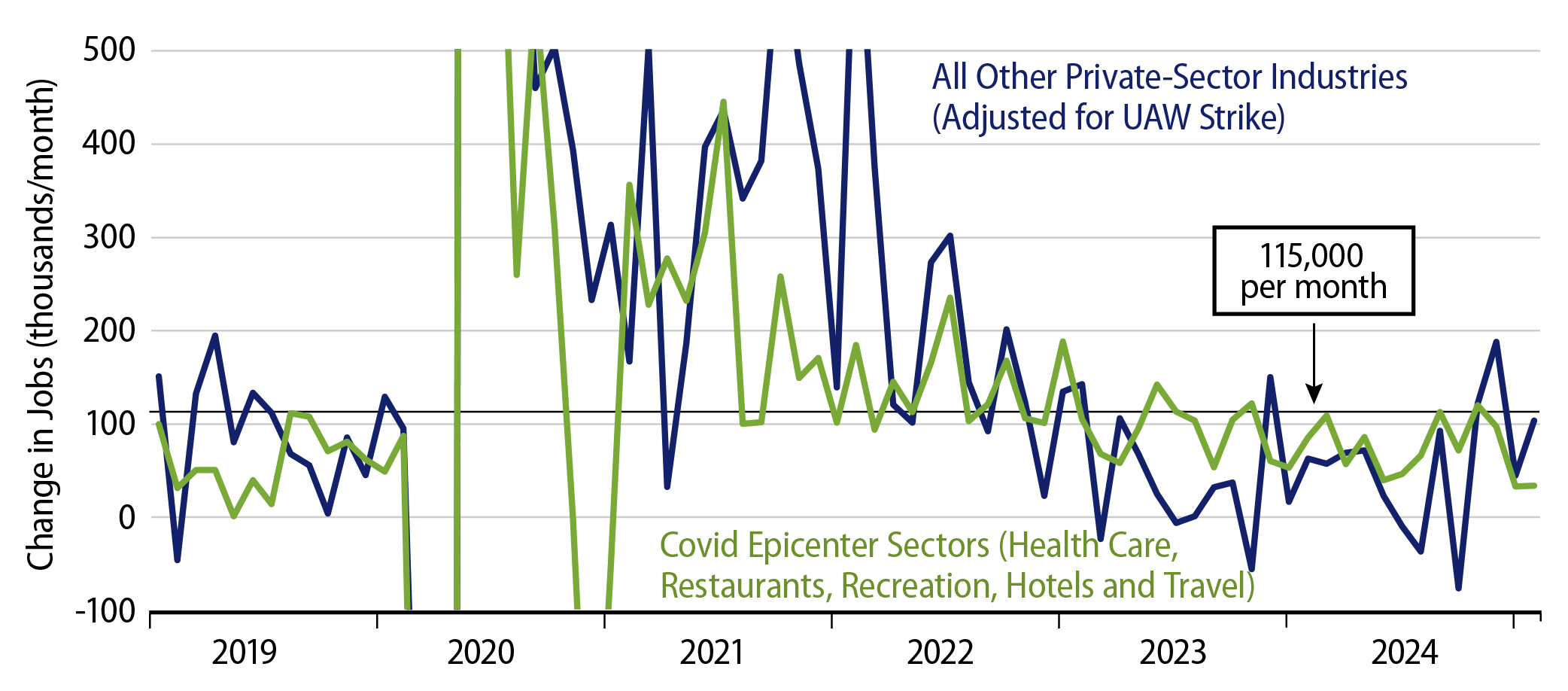

We have consistently decomposed the jobs data between sectors especially hit by the Covid shutdown of 2020 and those not so hard hit. From that perspective, the recent data show slowing growth in Covid-affected sectors, while other sectors have seen a modest bounce in job growth. Exhibit 1 illustrates these details.

The slowing in Covid-sector job growth has occurred as health care job growth has ticked down slightly, from 55,000 per month in late-2024 to 45,000 per month so far this year, and as restaurants have swung from adding jobs to shedding them. For the ''non-Covid'' sectors, the recent improvement has mostly been in finance and logistics.

As is clear in the chart, both broad groups have shown slower job growth lately than was seen pre-Covid, and the accompanying declines in workweeks also cast a pall on the job growth pace. That said, there is no clear declining trend in job growth for either broad group lately, and recent job growth rates are not slow enough to smack of actual weakness in the economy; rather, they suggest mere sluggishness.

Still, the Fed likely does not want to see job growth slowing further. That concern and modest wage growth should combine to nudge the Fed to further rate cuts. This is provided, of course, that an onslaught of tariffs—and related price hikes—doesn’t throw a monkey wrench into those designs.