Private-sector payroll jobs rose by 111,000 in January, according to data released today by the Bureau of Labor Statistics (BLS). The release also featured benchmark revisions of the employment data, which resulted in a -621,000 revision to the private-sector jobs data through March 2024. There are a lot of moving parts within these data, so let’s take it slow.

The original payroll data we get are based on a monthly survey of payroll establishments, which typically cover only a portion of the private sector (something like 40% of employers and 60% of employees). Eventually, more complete payroll information is available when quarterly payroll tax returns are submitted, and those data are fully compiled by BLS. The benchmark revisions released today are based on full payroll tax data through the March 2024 returns.

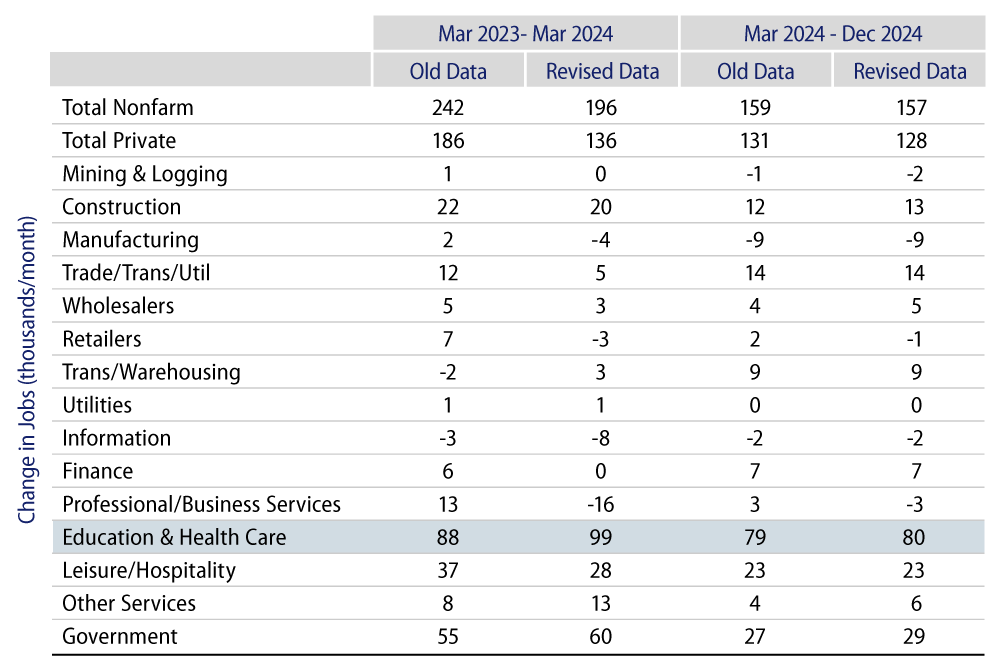

While large, the -621,000 revision is actually smaller than the -819,000 revision for that data that BLS originally projected last summer. The revisions do imply much slower job growth than the preliminary data indicated, and there is an ongoing slowing trend in job growth detectable in these data. More to the point, the revised data show that most of the job growth over the last two years has been focused in one particular sector/industry, private education and health care. (This sector also includes ''social'' assistance, such as nursing care, child care and social work.)

This sector comprises about 20% of private-sector employment. However, it has accounted for 69% of total private-sector job growth over the 21 months through December 2024. Looking at health care alone, it accounts for 13% of total private-sector jobs, but 44% of job growth over those 21 months.

In other words, while health care and related fields show continued resilient growth, growth has slowed to a sputter across the rest of the economy. Exhibit 1 shows sector details for revisions and recent growth rates.

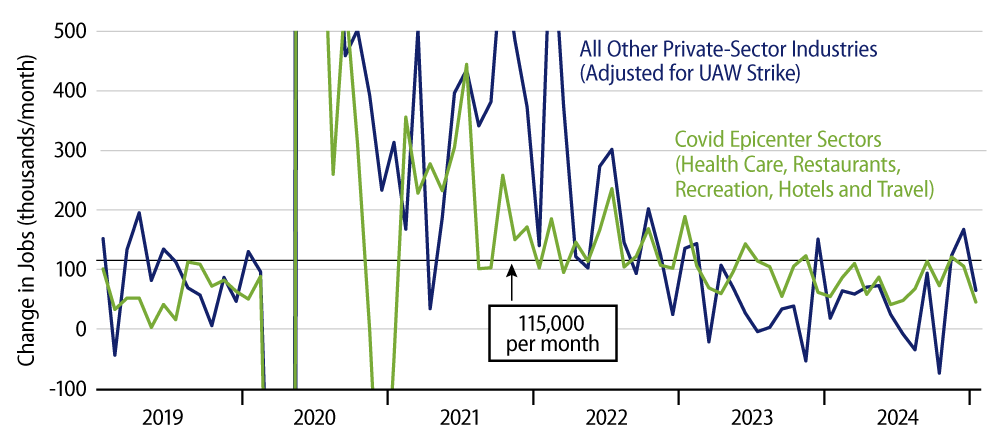

In past posts, we have emphasized the differences in job growth between sectors especially hard-hit by the Covid shutdown (''Covid epicenter'' sectors in the charts), and the rest of the economy. Exhibit 2 shows the near-zero growth in these sectors since mid-2023, prior to a recent spurt. However, that ''spurt'' is mostly a rebound from hurricane-related job losses over July to October. In that chart, you can also clearly see the especially soft job data during hurricane months. Looking at the last seven months overall, in order to average out hurricane and post-hurricane months’ tallies, overall private-sector jobs are about 53,000 (cumulative) higher than what would have occurred had pre-July trends been recently sustained. That is within the range of measurement error.

In other words, what looks like a recent upturn in job growth is more likely statistical noise caused by the hurricanes. And, no, the economy is not dropping off a cliff. However, job growth remains very soft in most of the economy, and even the roaring growth in health care and related sectors merely brings total growth to mediocre rates.