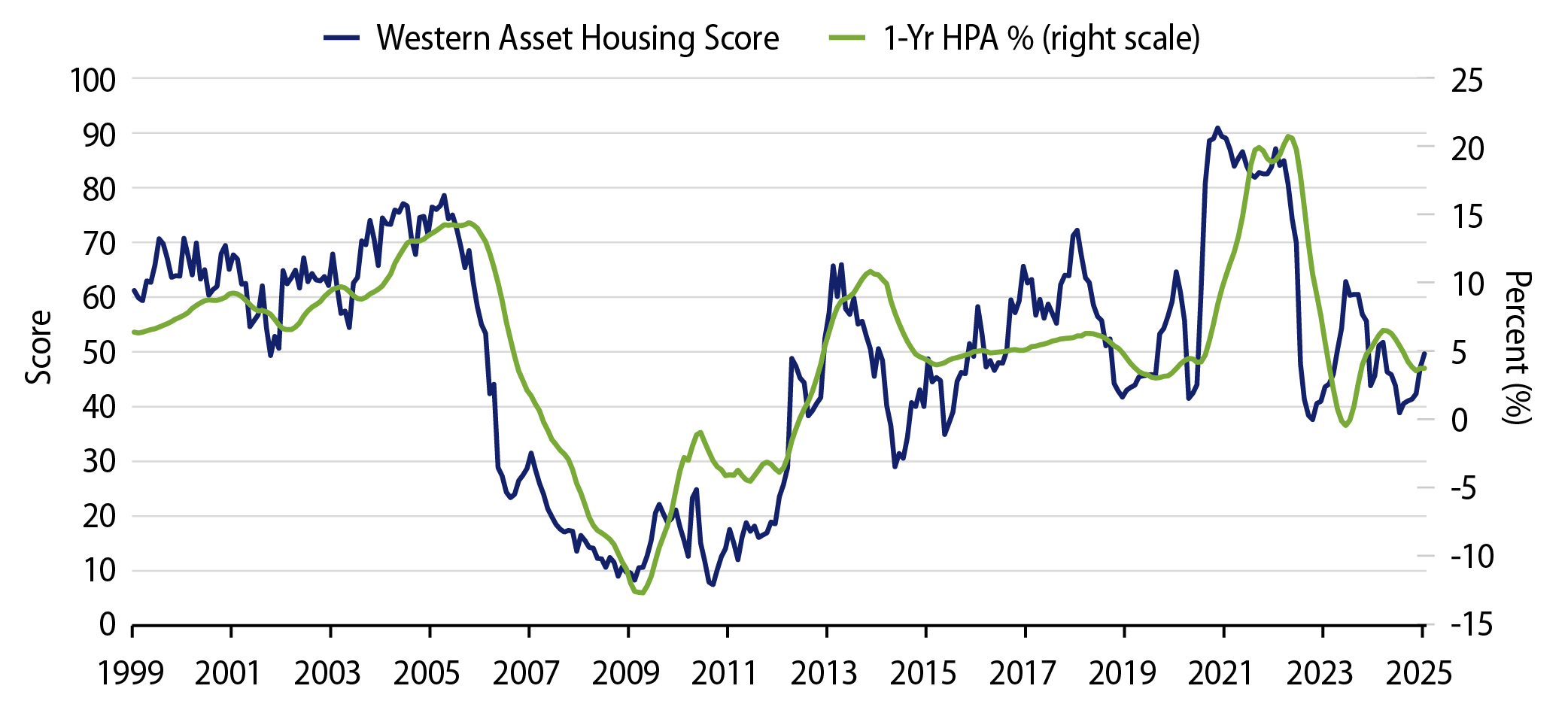

The Western Asset Housing Market Score has a current value of 50, which corresponds to an annual home price appreciation rate of 4.9% based on our model. The score has gradually risen since August 2024 but saw a significant uptick in December and January. Two main drivers have helped to increase the score: (1) the months of existing-home supply declined to 3.3 months from the mid-4s, and (2) home builder sentiment, based on prospective buyer traffic, is at its highest level since April 2024.

As we start 2025, the themes that we see in the housing market are much the same as those seen last year. The current 300-basis-point spread between the prevailing 30-year conforming mortgage rate of about 7% and the average rate on outstanding mortgages of about 4% continues to exacerbate the “locked in” effect that has been prevalent since the Federal Reserve started raising rates a few years ago. The monthly payment impact related to rates rising from 4% to 7% has prevented and continues to prevent homeowners from putting their existing homes on the market to buy another existing or newly built home. All of this has driven housing turnover to the lowest levels seen since 1981. Our perspective is that the longer mortgage rates stay at their current levels the more “normal” they become and, ultimately, that consumers must bite the bullet and make housing moves. However, it’s hard to predict when that will happen in any meaningful way to unlock the market.

In terms of borrowers’ performance, fundamentals have remained strong but are worth further scrutiny. As reported by the Mortgage Bankers Association, delinquencies as a percentage of outstanding loans ended 2024 at 3.98%. This is the highest reading since the first quarter of 2022. While historically low, the directionality of the move indicates that delinquencies are on the rise. As time moves forward and the trajectory of equity gains that borrowers have enjoyed over the past few years slows, highly levered borrowers could stumble.

Performance measures continue to be positive and provide strong fundamentals to securitized residential credit. We continue to like strongly underwritten deals where loan-to-value ratios are 70%-80% and are paired with slightly out-of-the-money mortgage rates. Overall spread levels remain at the tighter end of the range, but opportunities still exist in the fixed-rate sectors of non-qualified mortgages (NQMs) and residential transition loans (RTLs). Credit risk transfer (CRT) bonds offer floating-rate risk but are limited in supply, which makes them both attractive and hard to source.

Given all these factors, we remain positive on US residential housing fundamentals. Home price appreciation on a national level is expected to remain subdued with annualized growth rates expected to be in the low single digits for the foreseeable future. We do not see a significant risk of defaults in the broad residential market.