We are excited to share that we just launched a new municipal strategies landing page designed to serve as a one-stop destination for all Western Asset municipal solutions and timely content.

Macros, Markets and Munis

The municipal market sold off sharply last week, with Treasuries moving 30-50 basis points (bps) higher across the yield curve while munis generally underperformed amid weak demand and elevated supply conditions. Market volatility spiked last week, and municipals experienced one of the most volatile weeks in history as equities sold off sharply and fixed-income yields moved higher amid heightened recessionary and inflationary fears associated with new tariff policies. Meanwhile, technicals were challenged by record outflows and the elevated supply. This week we highlight the record volatility observed last week in the muni market and attractive income opportunities.

Fund Outflows Accelerated Amid Broader Market Volatility

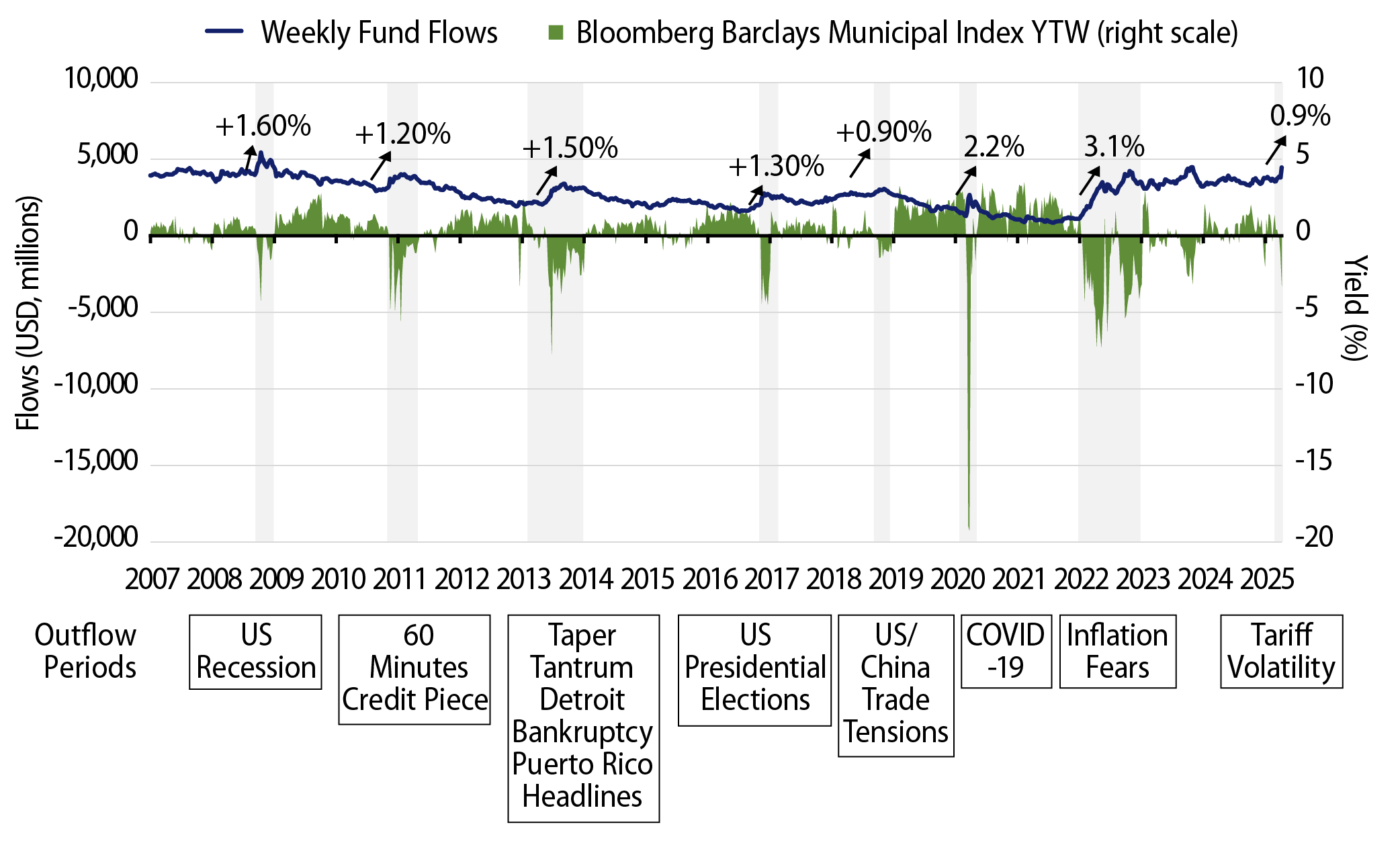

Fund Flows (down $3.3 billion): During the week ending April 9, weekly reporting municipal mutual funds recorded $3.3 billion of net outflows, according to Lipper. Long-term funds recorded $2.6 billion of outflows, intermediate funds recorded $297 million of outflows and high-yield funds recorded $759 million of outflows. Last week’s outflows represented a record weekly outflow level and led year-to-date (YTD) inflows lower to $7 billion.

Supply (YTD supply of $141 billion; up 33% YoY): The muni market recorded $8 billion of new-issue supply last week, down 39% from the prior week. YTD, the muni market recorded $141 billion of new issuance, up 33% year-over-year (YoY). Tax-exempt and taxable issuance are up 33% and 34% this year, respectively, though tax-exempt issuance has comprised the vast majority (95%) of YTD supply. This week’s calendar is expected to increase to remain elevated at $12 billion. The largest deals include $1.75 billion taxable New York City General Obligations and $1.6 billion Connecticut General Obligation transactions.

This Week in Munis: Unprecedented Volatility

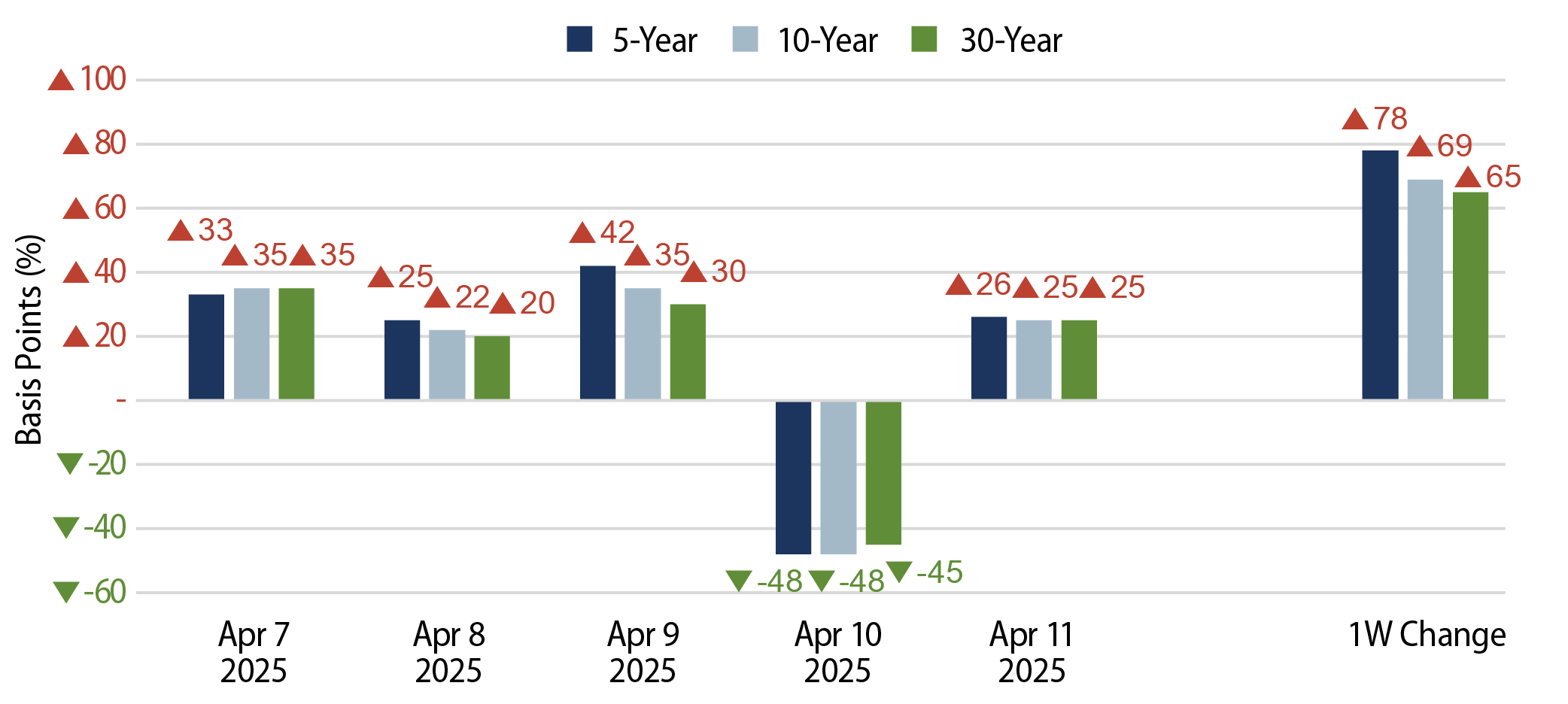

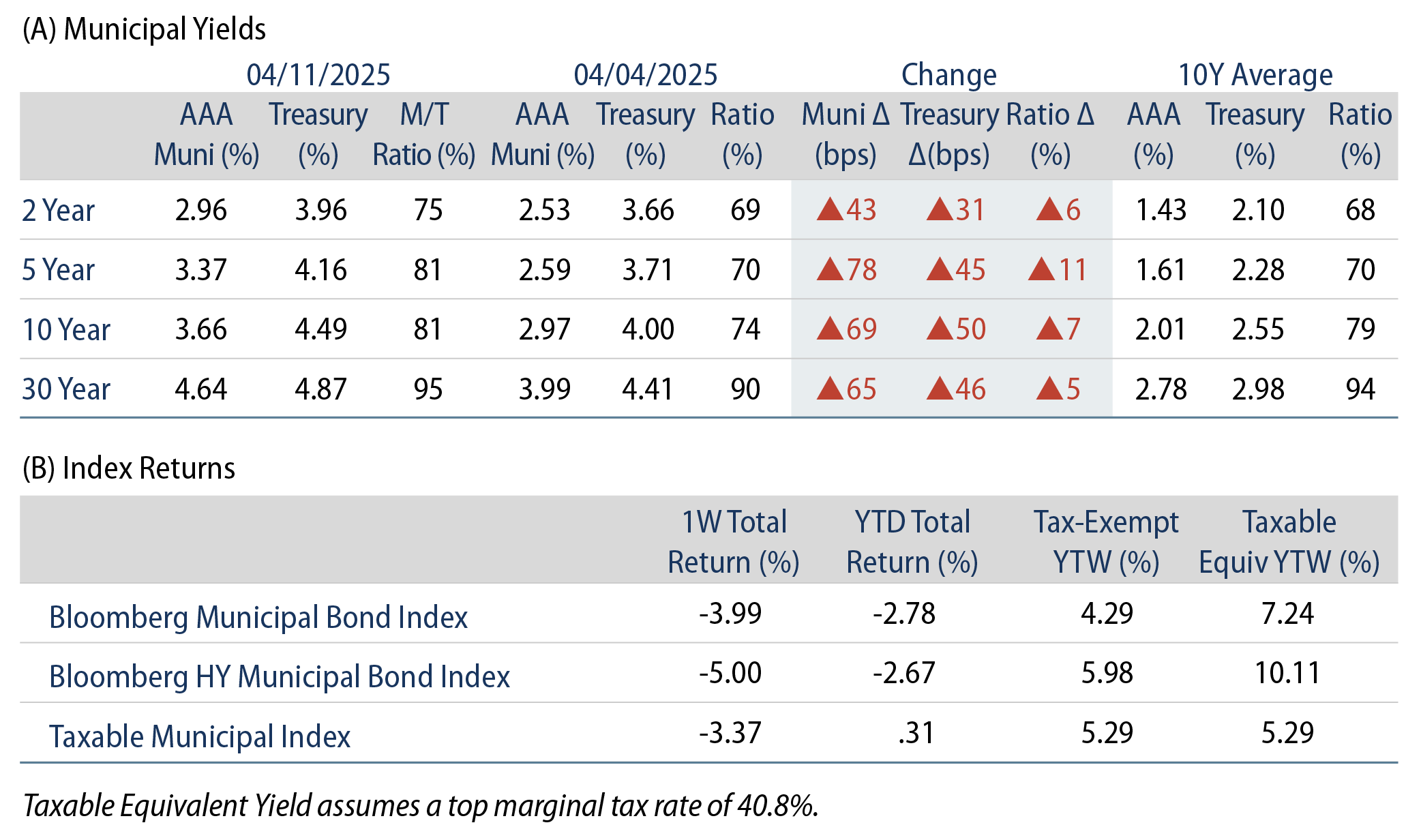

The municipal market experienced unprecedented volatility last week. AAA Municipal Market Data (MMD) Index yields moved up by 20-42 bps each day from Monday to Wednesday, before dropping sharply by 45-48 bps on Thursday, only to rise again by 25-26 bps on Friday. All told, the AAA municipal yield curve had increased by 65-78 bps higher during the week, exceeding the 45-50-bp rise observed in commensurate maturity Treasury yields.

Western Asset does not consider the recent tariff measures to be a widespread negative credit event for most municipal market issuers; instead, we attribute the significant price volatility to liquidity challenges. The municipal bond market is fragmented and typically experiences relatively limited trading activity, which can lead to underperformance during periods of short-term market volatility. We believe that a confluence of rate volatility, rebalancing associated with equity market drawdowns, and tax season selling pressures all contributed to the weekly record $3.3 billion fund outflows and relative weakness during the week.

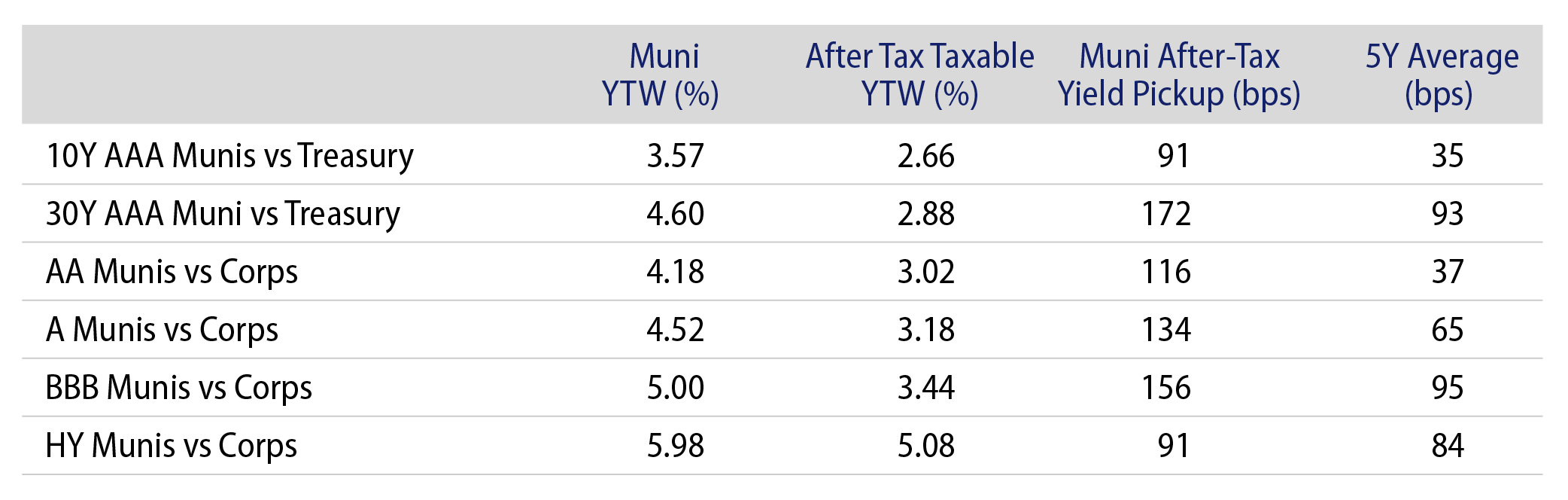

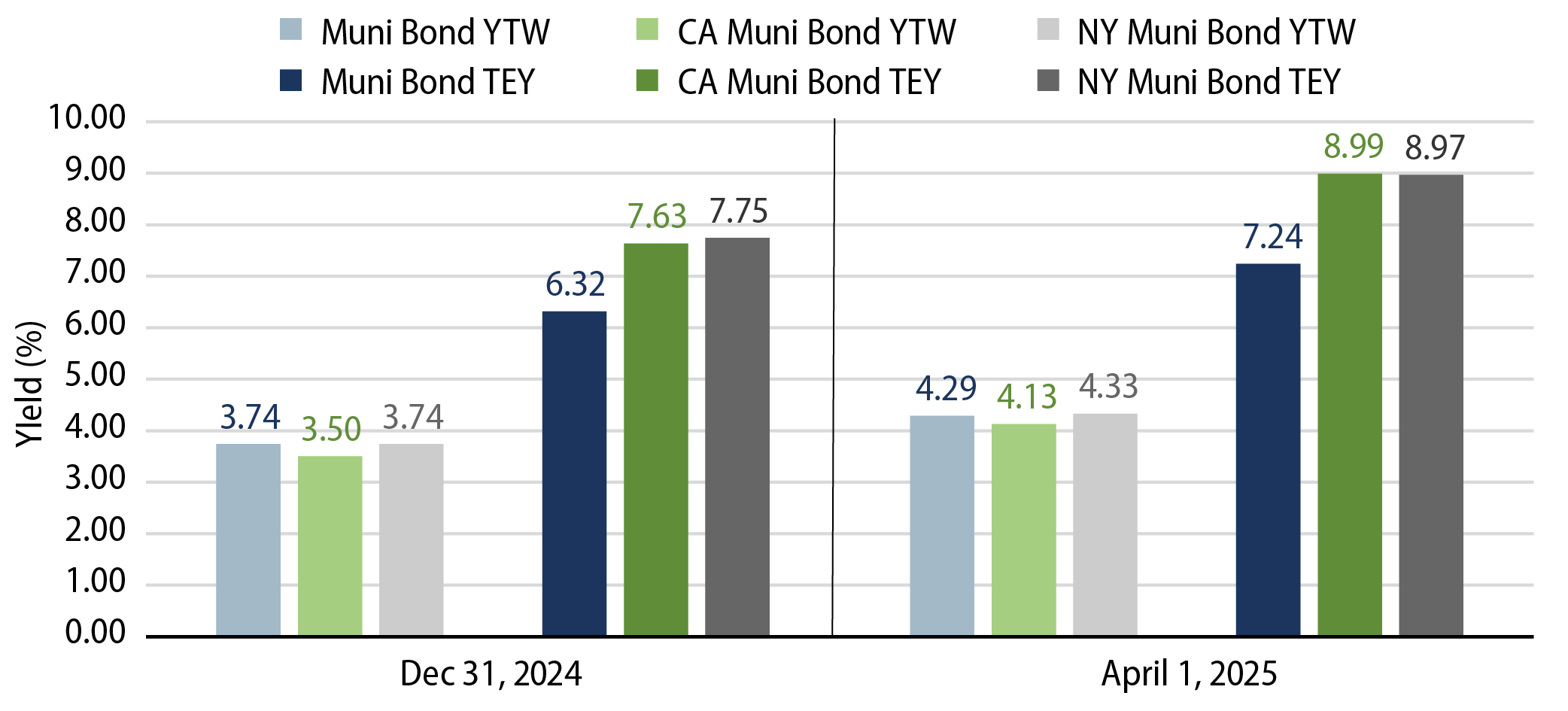

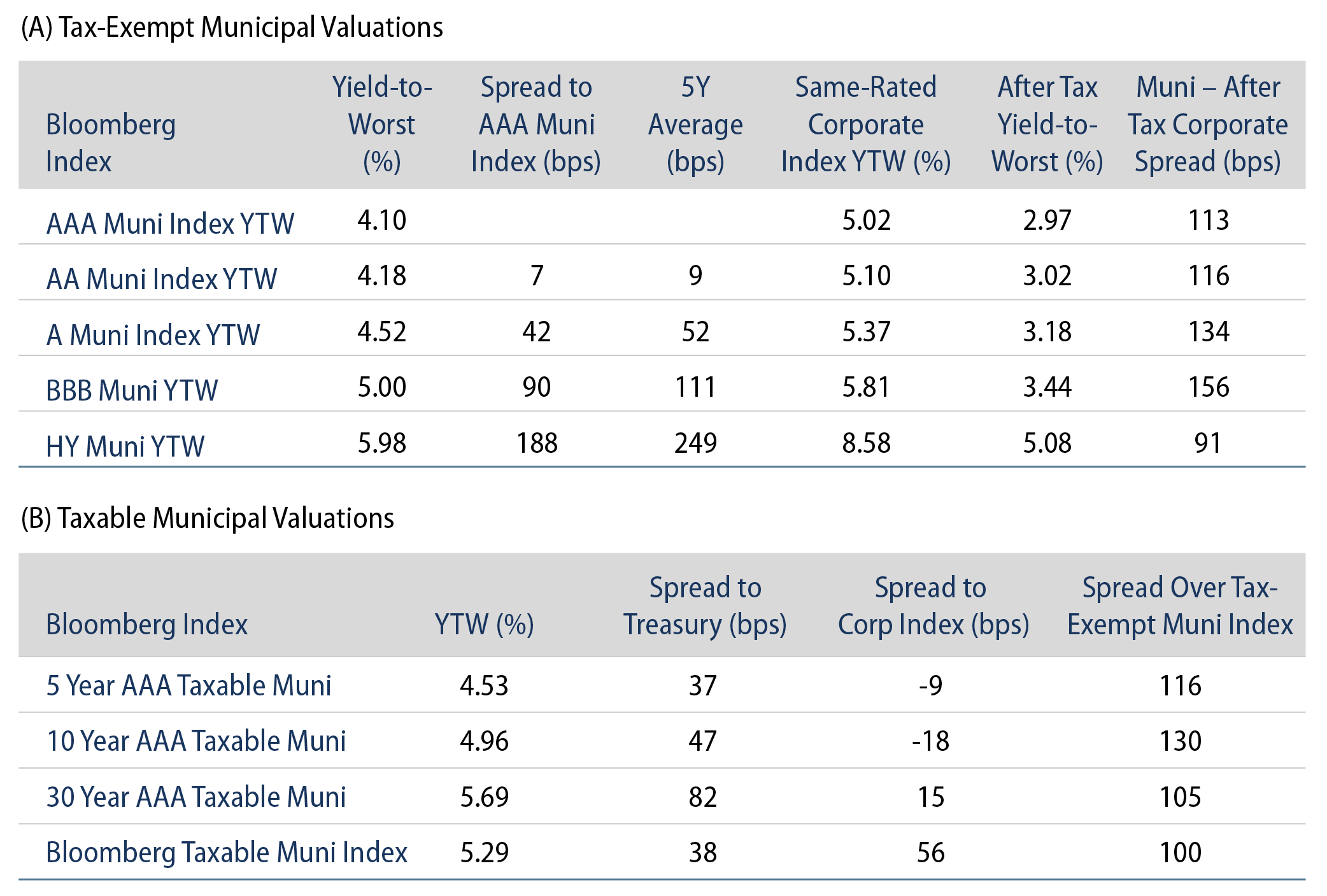

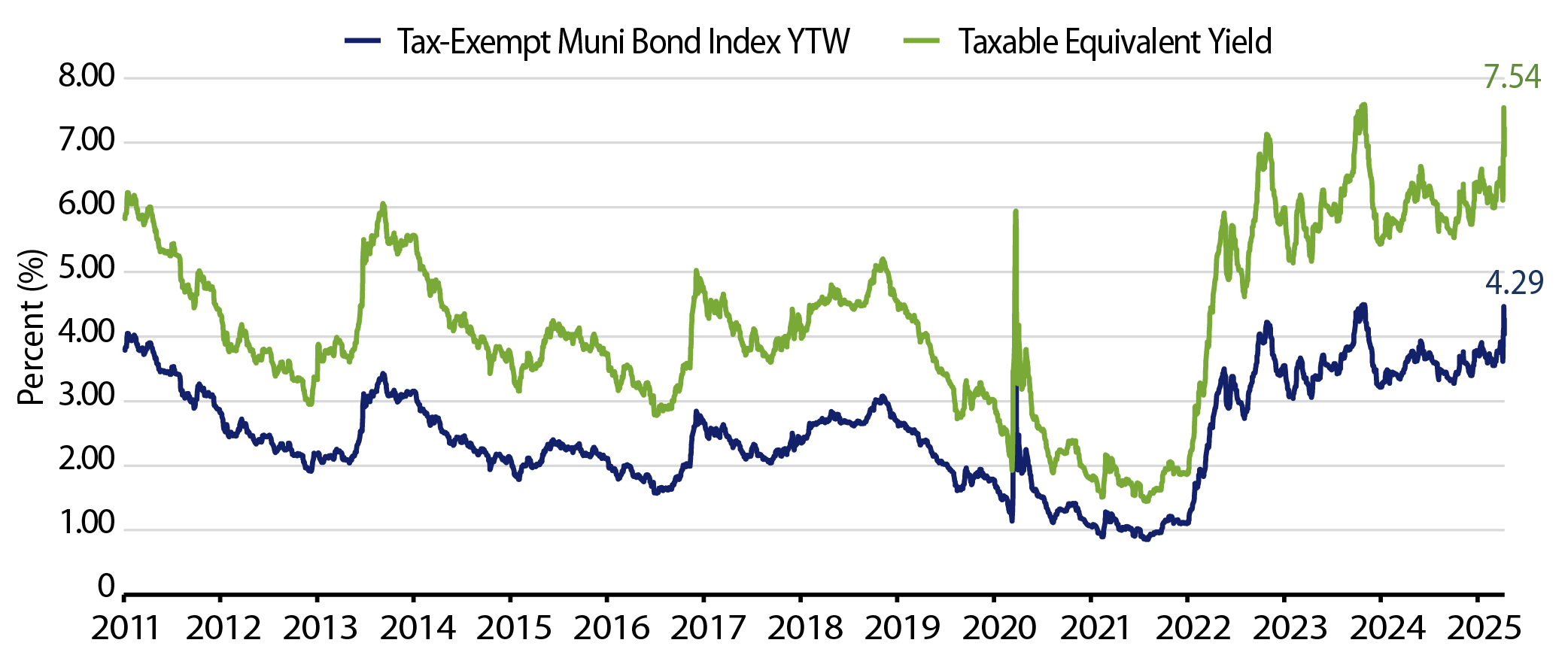

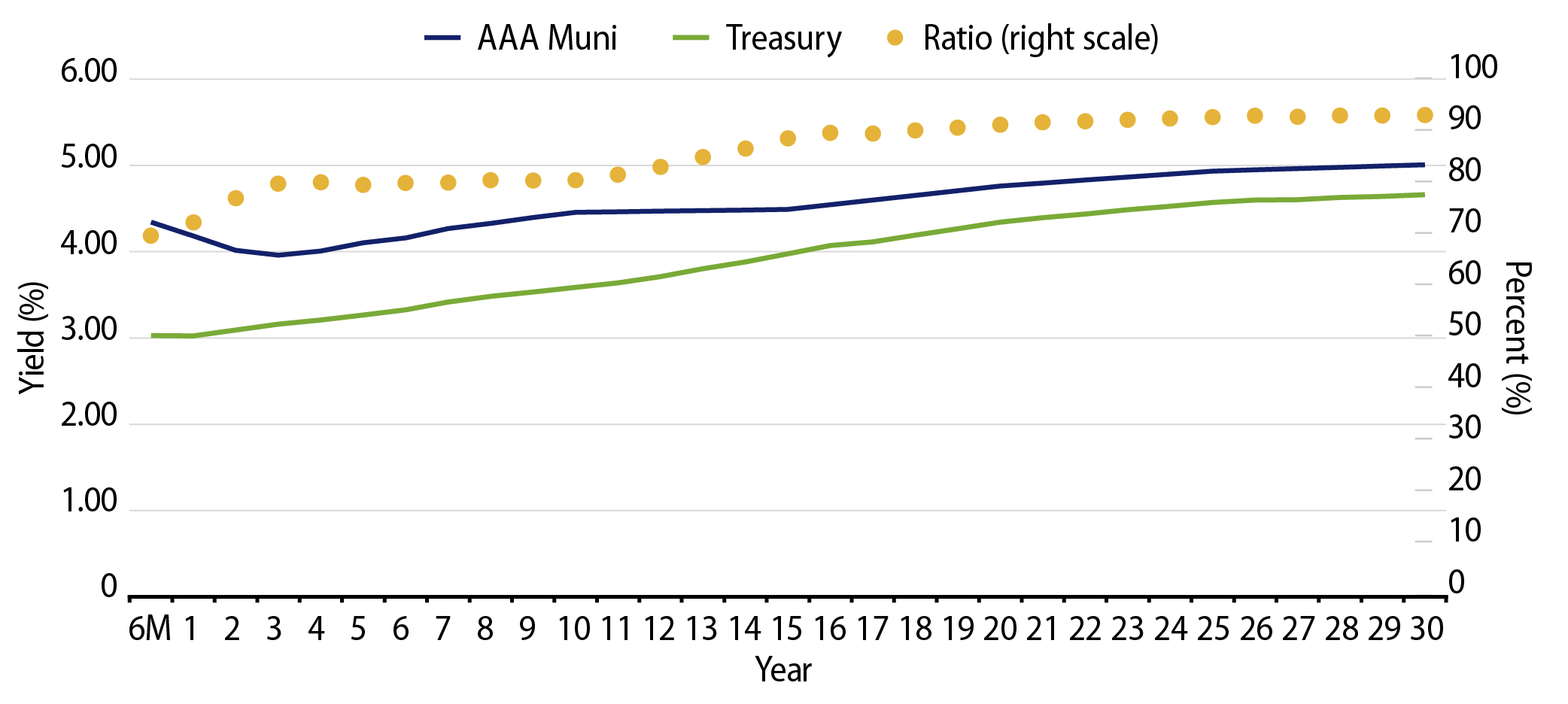

Liquidity events in the municipal market have historically contributed to attractive tax-exempt income opportunities and the potential for longer-term after-tax outperformance. This week, the yield on the Bloomberg Municipal Bond Index increased by 67 bps to 4.29%, enhancing tax-adjusted income opportunities. For the highest bracket of taxpayers, the average taxable equivalent yields in New York and California approached 9.0%. Additionally, when considering only the top federal tax rate, 10-year AAA municipal securities now offer 91 bps of excess yield pickup compared to Treasuries, while BBB municipals provide 156 bps of after-tax yield pickup compared to BBB corporates. Given our expectation that municipal credit fundamentals are likely to remain sound, we believe this represents an attractive risk-adjusted value opportunity, especially in light of the broader market volatility.

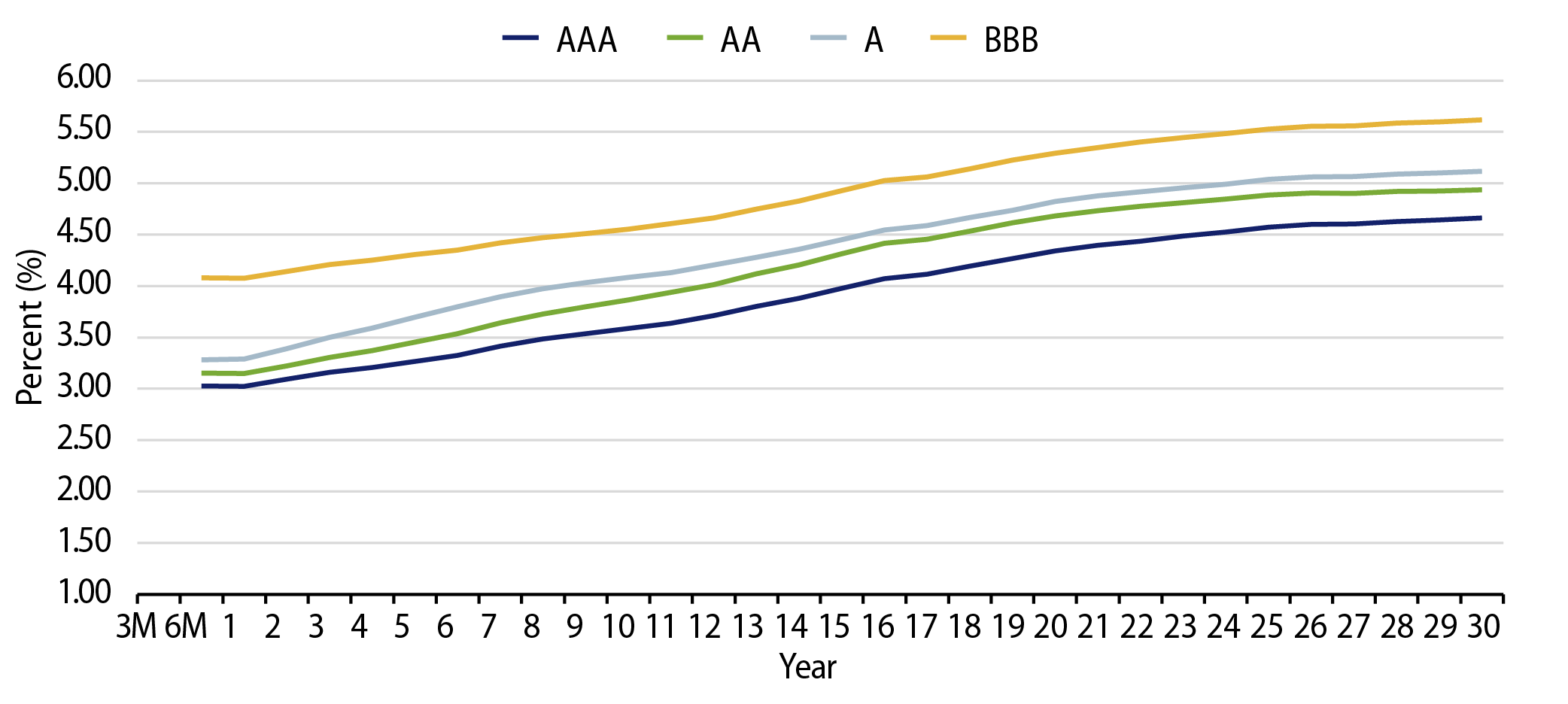

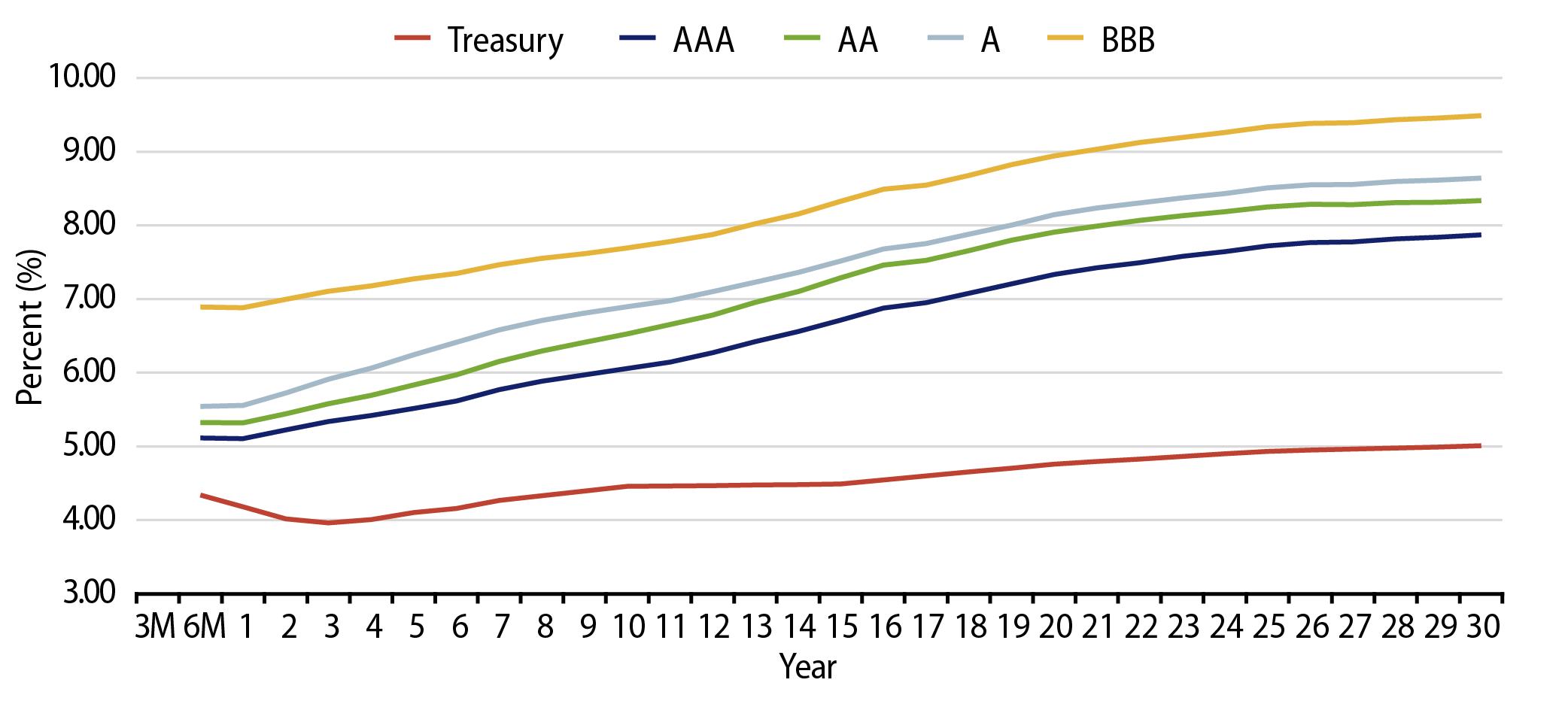

Municipal Credit Curves and Relative Value

Theme #1: Municipal taxable-equivalent yields and income opportunities spiked to decade-high levels.

Theme #2: The muni curve has steepened, offering better value in intermediate and longer maturities.

Theme #3: Munis offer attractive after-tax yield pickup versus longer-dated Treasuries and investment-grade corporate credit.