The Census Bureau reported today that sales of new single-family homes rose +7.4% from their February level. Last week, we learned that single-family housing starts declined -14.2% in March. Despite the large-sounding magnitudes of these swings, neither appears to indicate a significant departure from previous trends, as can be seen in Exhibit 1.

Homebuilding activity dropped substantially in 2022, when the Federal Reserve first began to raise interest rates and when the flurry of a post-Covid housing boomlet subsided. Since then, activity has held generally steady. Truth to tell, we have been looking for a further softening in activity, but it has not emerged.

Inventories of unsold new homes are quite high, equivalent to eight months’ worth of sales. In Exhibit 1, we have staggered the scales for single-family starts and new-home sales to account for coverage differences. (For one thing, owner-builds show up in starts, but not in sales.) The intent here is that when the blue line lies above the green line, new-home inventories are rising, and vice versa.

This is indeed the case. Yes, inventories of unsold new homes have been rising essentially nonstop for the last four years. However, builders have not yet felt compelled to reduce home production, even with inventories holding above eight months’ sales nearly nonstop for the last three years, compared to “normal” levels of four to five months’ sales. Nor have new-home sales put further pressure on homebuilding by dropping still lower despite ongoing increases in mortgage interest rates and already-high home prices.

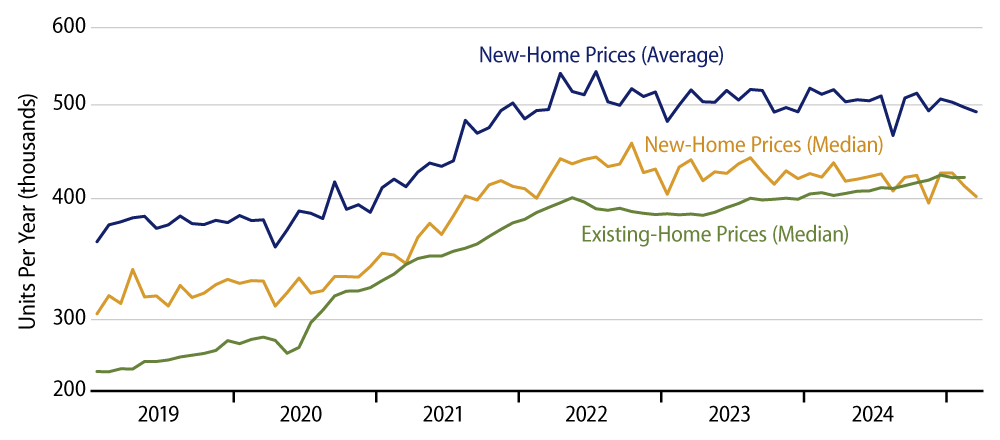

One concession builders have made is to offer some relief on home pricing. As seen in Exhibit 2, both median and average sales prices for new homes have been trending lower since mid-2022. No, new-home sales prices are not plummeting, but they are substantially underperforming compared to prices of existing homes, which continue to show some uptrend.

Some analysts contend that there is substantial pent-up demand for housing, thanks to supposed under-building during the 2010s. We don’t find this assertion particularly convincing. Then again, with homebuilding and sales levels sustaining recent levels despite very low affordability for prospective buyers and despite our own expectations of further weakening, a bit of circumspection is in order.

Once again, all in all, housing activity is not buoyant, but it has held up better than expected, and the recent data continue to indicate that.